The Japanese Juggernaut Rolls On

Topics

Plus ça change, plus c’est la même chose. — French expression

They don’t make much money, but they sure make a lot of stuff. — Down East Maine expression

Rumors of my demise have been much exaggerated. —Mark Twain

After years of observing U.S. industry under siege from foreign competitors, U.S. managers, shareholders, and business journalists have changed their mood from deepest gloom to near-euphoria. U.S. companies are reporting record profits, while the Japanese barely break even. Honda no longer has the best-selling auto model in North America, market share in the domestic U.S. vehicle market is no longer being eroded by Japanese firms or their U.S. transplant subsidiaries, and Chrysler has novel problems arising from a seemingly huge cash mountain. The Japanese invasion in personal computing and software has been conspicuously absent; indeed, there are few sectors of world business in which U.S. firms today are more dominant. And the once feared disappearance of the U.S. semiconductor industry has been replaced by dominance in microprocessors and even a respectable comeback in basic “chips.”

If these company and industry successes are not enough to demonstrate a comeback, the United States is experiencing robust economic growth, while Japan struggles with a protracted, unprecedented postwar recession. U.S. firms are leaner and meaner. “Quality” is no longer a Japanese monopoly. Moreover, the dollar is far down and the yen is up. Ergo, U.S. firms are more competitive than they have been in a decade or two. The Wall Street Journal has pronounced “America ascendant.” The World Economic Forum has declared “America on top.” The U.S. National Association of Manufacturers has weighed in with nearly as triumphant a tone. And The Economist, with only slightly greater uncertainty, heralds “the fading of Japanophobia.”1

World Market Shares

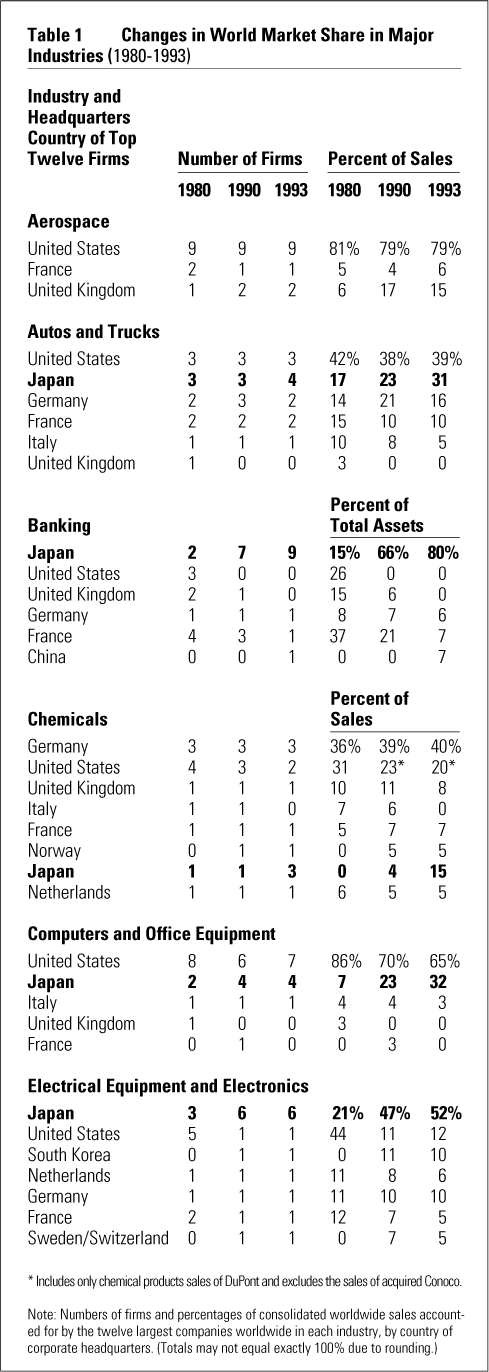

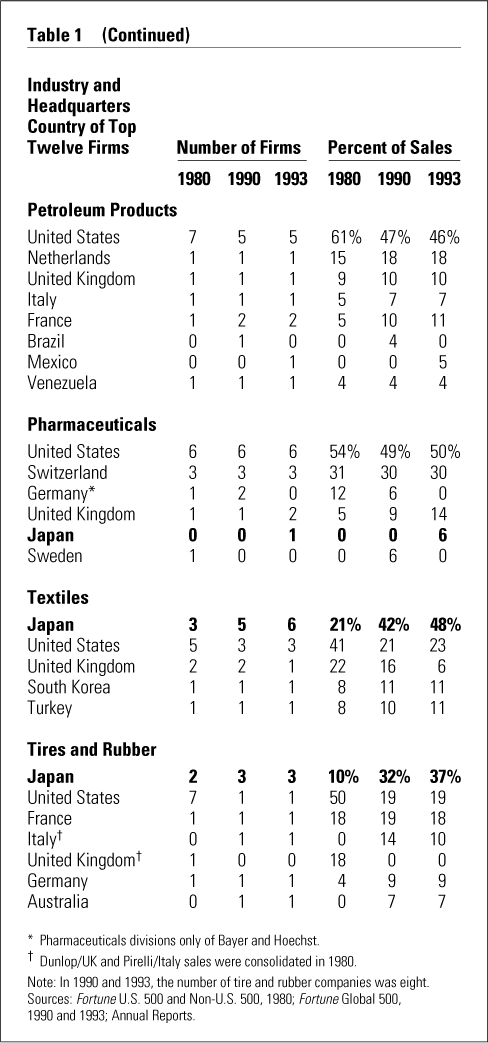

In light of all this good news for U.S. industry, we might expect to see noticeable reversals in the continual gains since the 1960s in major Japanese firms’ shares of world markets in industries such as autos and trucks, chemicals, computers and office equipment, electrical equipment and electronics, iron and steel, nonelectrical machinery, textiles, and tires and rubber. An avid reader of the business and financial press, I expected to find those reversals when I updated (through 1993) the company-based data I had been using to track changes in world market shares in these and other industries since 1960.2 But “the end of the Japanese challenge” is not the story that these numbers tell (see Table 1).

{kind=link}

Of course, there were U.S. company successes in the early 1990s. U.S. aircraft firms — and especially Boeing and United Technologies — maintained their dominance in aerospace, with a constant 79 percent world market share despite the near-eclipse of McDonnell-Douglas by the European Airbus consortium’s civil aircraft. (This is represented in Table 1 by France’s Aerospatiale and Britain’s British Aerospace.) Food processing and beverages, paper and forest products, pharmaceuticals, and, to a lesser extent, petroleum products remain very much U.S.-dominated industries.

The long erosion of U.S. auto companies’ world position, or at least Ford’s and Chrysler’s, appears to have ceased — or at least paused. General Electric has held its own against world competitors and, having transferred the headquarters of some product divisions to Asia, appears poised to continue. U.S. textile companies have retained a bit more than one-fifth of their industry share worldwide. And Goodyear, the United States’s one remaining world competitor in tires has also maintained its position.

Still, notable U.S. losses in world market share continued in computers and office equipment and in nonelectrical machinery. Primarily, these were losses to the Japanese. Moreover, Japanese firms had significant gains against all major Western competitors between 1990 and 1993 in world market shares not only in these two sectors, but also in autos, chemicals, electrical equipment, iron and steel, textiles, and tires. The Japanese challenge, on a global if not North American scale, thus seems to be thriving in the 1990s, albeit largely at the expense of European firms’ positions.

Japan’s Invisible Challenge?

If the Japanese challenge has not gone away, and if indeed there have been several major Japanese market share advances during the early 1990s, why haven’t they been more visible? Of course, part of the Japanese challenge continues to be visible. Despite all the comebacks of “lean and mean” U.S. firms and a strong yen, the United States is running a huge trade deficit with Japan. And, although a trade deficit per se is an indicator not of company “competitiveness” but of imbalances in Japanese and U.S. consumption versus savings, the sectoral distribution of the deficit —skewed to autos and parts, computer peripherals, and electronics and electrical equipment — is indicative of Japanese companies’ capabilities in those industries. Perhaps the main reason for the “invisibility” of the Japanese challenge to North American — and even some European — observers is that the financial press is very impressed with companies whose share prices are going up and whose profits are high, and very unimpressed with firms with declining or stagnant share prices and minimal margins.

The (mis)use of share price movements as an indicator of Japanese firms’ success, failure, or competitive position relative to U.S. or European firms is worthy of a lengthy discussion on its own. Suffice it to say here that, for Japan, the stock-price measuring stick is bent vastly more than usual. In particular, Japan’s late 1980s “bubble economy” ballooned share prices to a stratospheric level that, even after six years of stock market decline and stagnation, is still being disinflated to something closer to what might be considered “realistic” in the West. Add in artificial stock market “supports” and “caps,” and Japanese share prices could well have only the loosest relationship to company or even economywide “real” results or prospects for some time to come. (The “supports” include banks’ and insurance companies’ reluctance to sell their shares in Japanese companies, as well as occasional government market stabilization schemes; the “caps” include the massive overhang of possible conversion from convertible bonds to shares related to huge equity-linked financing of Japanese firms in the Euro-markets during the 1980s).

As for the usual financial measures of “performance,” the majority of Japanese industrial companies are currently reporting shrunken margins and tiny returns on equity, as might be expected of firms based in a home market mired in a prolonged recession and facing a soaring currency. The strong yen, in particular, compresses the margins of Japanese industrial firms by pushing down the relative prices (in yen) of Japanese exports and of locally produced goods and services that compete with imports. Even so, Japanese companies’ ROEs of 5 percent or so are not as small as they look to Western eyes. Quite apart from accounting conservatism, these ROEs are achieved while the yen economy is undergoing price deflation and yendenominated bonds yield some 2.7 percent.

Moreover, compressed margins and limited profitability are valid indicators of long-term competitive position only if they limit firms’ abilities to increase global sales and gain world market share relative to competitors. Most Japanese industrial firms have reached no such limit. Let’s first consider sales made to world markets from Japanese factories. Despite the strong yen, Japanese export volumes and yen values increased in most industries between 1990 and 1992 (see Table 2). Faced with recession at home, Japanese firms kept their plants running by exporting more. Not only did the stronger and stronger yen not deter exports, but it is arguably the case that much of the causation ran the other way: increased Japanese exports priced to sell in international markets increased the demand for Japanese goods and the yen needed to buy them. Contrary to the view that the yen is grossly over-valued at 80 or even 100 to the dollar (the result of most calculations of purchasing power parity [PPP], even those using producer price indices that include mostly internationally tradable goods), estimates of PPP based on Japanese export prices suggest no significant overvaluation.3

{kind=link}

Parenthetically, the fact that Japanese export volumes increased despite the strong yen substantially attenuates the possibility of currency effects warping the conclusions of the dollar-equivalent numbers in Table 1. It could be argued that some (or all) of the Japanese gains indicated by one measure of world market share, the consolidated value of the top twelve firms’ worldwide sales (including home, export, and foreign-produced sales) in U.S. dollars in each industry, could have been due to currency changes between 1990 and 1993. The yen could indeed buy some 20 percent more dollars at the end of 1993 than it did at the end of 1990. But Japan’s export volume gains in most of the industries I surveyed, along with continued healthy increases in direct foreign investment (DFI) by Japanese firms, argue that the continuing Japanese industrial challenge is no mere currency illusion. Moreover, those export and DFI increases behind the Japanese gains in world market share were “invisible” to many Western eyes for yet another reason: the Japanese challenge, aimed at the United States and Western Europe before and during the 1980s, has now turned to Asia (see Figure 1).

{kind=link}

Japanese exports to the United States grew in dollar terms some 25 percent in the early 1990s (implying roughly constant export volumes in yen), increased little to Europe, but increased by 70 percent or more since 1990 (and by 150 percent since 1985) to Asia. Indeed, “Asia overtook the United States as Japan’s largest export destination in 1991 and last year [1993] Japan’s trade surplus with the region surpassed its surplus with the United States for the first time. Ten years ago, Japan exported a third more to the United States than to Asia; now the balance is the other way.”4

The proportion of Japanese DFI in Asia has also now surpassed that in Europe. In 1990, it was running at half that in Europe. The Asian proportion of the annual Japanese DFI flow is now close to half that going to North America; in 1990, it was around one-seventh. (The change in this latter proportion is partly due to a dramatic decrease in DFI flows to the United States — following Japanese disenchantment with the returns on U.S. real estate and film studios — in addition to an absolute increase in Japanese DFI flows to Asia.)

Difficulties, Not Demise

How could Japanese corporations continue to gain world market share while having minimal profitability? Part of the answer lies in the word “cash.” Cash is necessary to carry out investments in global sales and direct investment development, and the leading Japanese firms not only have no cash shortage, but in many cases have “yen to burn.”5 Consider the liquid cash assets of Toyota ($25 billion), Hitachi ($24 billion), Matsushita ($22 billion), Canon ($6 billion), Fuji Photo Film ($6 billion), and Sony ($6 billion) — all but the last with balance sheet and financial strength ratings by Value Line of “A” to “A++.” (Sony, the only one of these to have a long-term debt-to-capitalization ratio of more than one-third, rates a mere “B+.”) The “highly leveraged Japanese firm,” at least in world industries, is largely a mythological creature of long ago.

Where is this cash coming from, if not from current profitability? It is from massive depreciation charges related to the similarly massive capital expenditures that Japanese firms undertook not only during the late 1980s “bubble economy” but also right through 1991. Indeed, several major companies (e.g., Canon) have not slackened at all.6

The R&D and Innovation Motor

Another part of Japanese companies’ “profitless prowess” is their continued R&D and innovation efforts.7 If 1991 marked a watershed in capital equipment expenditure, it did not affect the Japanese companies’ R&D efforts leading to productivity increases that have given Toyota, for example, a break-even exchange rate of 50 yen to the dollar (see Table 3). Reductions in Japanese R&D that might have enhanced reported profit are rare between 1990 and 1993; more frequent are increases in absolute R&D spending levels (measured in dollars) that exceeded the 20 percent revaluation of the yen.

{kind=link}

Consider also the Japanese corporate position as measured by U.S. patents. A 1993 Business Week ranking (for 1992) of the world’s twenty-five largest companies by “strongest U.S. patent portfolios” placed twelve Japanese companies on the list, compared to ten U.S. firms, two German firms, and one Dutch company. The top three holders of numbers of U.S. patents were Canon, Hitachi, and Toshiba.8

U.S. Business’s Response

The message in this survey is no mystery. The rebounding profits of corporate America should be no cause for U.S. managers’ complacency. Rumors of the demise of the Japanese competitive challenge have been greatly exaggerated. Profitability is not the same thing as “competitiveness.” U.S. corporate profits in world industries have recently been magnified by a perhaps temporarily weak dollar and strong yen. But current profitability is a much poorer yardstick for judging competitive position than are the measuring rods of world market share, cash flow, and corporate innovation capabilities. Moreover, Japanese profits could rebound with unexpected rapidity. Stranger things have happened to currencies than, say, a rise in the dollar that might follow any real effort to reduce the U.S. government budget deficit and increase the U.S. savings rate, or a weakening of the yen that would come from a less deflationary Japanese monetary policy. Were such currency events to occur, the world would be amazed at the dramatic, “surprising” boom in Japanese corporate profitability.

How can U.S. companies respond appropriately to the continuing Japanese global challenge? One stunningly inappropriate response is for companies to support U.S. government efforts to improve U.S. market shares by bludgeoning, as in the current U.S. administration’s attempt to open an allegedly closed Japanese automobile and parts market via highly public threats of sanctions, quotas, and so on. Not only can the Japanese easily and subtly retaliate by, say, buying more Airbuses and fewer Boeings —thus shifting the market shares in different sectors around a bit — but for U.S. interests to expend such effort and emotion fighting for a marginal piece of a mature, if not stagnant Japanese home market is a remarkable case of “fighting the last war.” The future markets for autos, parts, and many other products (and services) are in the emerging markets of Asia. Bringing out the big battalions to “attack Japan” will do nothing to solve the real and future problem of how U.S. and European companies can avoid being preempted in Asian markets by Japanese firms. In many of these markets, the Japanese are well ahead. Detroit should worry less about lack of market share in Japan and more about the lack of share in Thailand, Malaysia, Indonesia, India, and China.

The real strategic question for U.S. and other Western firms is whether they are matching or exceeding the worldwide thrust of the Japanese. Or are U.S. firms just using the current dollar weakness mainly to enhance today’s reported profit and dividend payout? Are U.S. firms keeping up with or beating the Japanese R&D and innovation efforts and positioning themselves in future world markets? Or are recent reports of major reductions in U.S. companies’ R&D more the norm? The competitiveness of U.S. firms in the coming global economy will depend on answers to these questions. If there are enough affirmative answers, perhaps the world market share tables for the year 2000 will finally show a halt in the more than thirty years of global decline in the world positions of too many U.S. and European companies. But if I were to place bets. . . .

References

1. R.T. King and S.K. Yoder, “America Ascendant: U.S. Companies’ New Competitiveness,” Wall Street Journal, 8 September 1994, p. A1, and 9 September 1994, p. A1;

“America on Top,” The Economist, 10 September 1994, p. 81;

E. Faltermayer, “Competitiveness: How U.S. Companies Stack up Now,” Fortune, 18 April 1994, pp. 52–64; and

“The Fading of Japanophobia,” The Economist, 6 August 1994, pp. 21–22.

2. L.G. Franko, “Multinationals: The End of U.S. Dominance,” Harvard Business Review, November–December 1978, pp. 93–101;

L.G. Franko, “Global Corporate Competition: Who’s Winning, Who’s Losing, and the R&D Factor as One Reason Why,” Strategic Management Journal 10 (1989a): 449–474;

L.G. Franko, “Unrelated Diversification and Global Corporate Performance,” in A.R. Negandhi and A. Savara, eds., International Strategic Management (Lexington, Massachusetts: Lexington Books, 1989b);

L.G. Franko, “Global Corporate Competition II: Is the Large American Firm an Endangered Species?” Business Horizons, November–December 1991, pp. 14–22.

3. Using 1973 as a base year, Goldman estimated a January–March 1994 PPP yen/dollar rate at ¥216/$ using consumer prices; ¥158/$ using producer prices; and ¥92.4 using Japanese export prices versus U.S. producer prices. See:

Goldman Sachs, “Japan Research: Research Review,” 18 July 1994, p. 4.

4. W. Dawkins, “When Neighbours Make Good Returns: The Yen’s Rise Is Encouraging a Strategic Shift by Japanese Industry into Other Asian Markets,” Financial Times, 15 July 1994, p. 13.

5. See “Cash Is King for Corporate Japan,” Business Week, May 1, 1995, p. 37; and Value Line, various issues.

6. For historical capital expenditure and cash flow patterns of the companies mentioned, see Value Line, various issues.

7. On the importance of R&D as a “driver” of long-term world market share, see: Franko (1989a).

8. “The Global Patent Race Picks Up Speed,” Business Week, 9 August 1993, p. 57.