Charting a Path Toward Integrated Solutions

For manufacturers and service companies alike, the ability to sell integrated solutions requires completely new organizational structures and capabilities.

Some of the world’s leading companies IBM, General Electric, Rolls-Royce, Ericsson, and EDS among them — now compete by providing integrated solutions rather than making stand-alone products or selling services.1

Suppliers of products as diverse as information technology systems, trains, aircraft engines and telecom systems have achieved success with this approach by providing innovative combinations of technology, products and services as high-value unified responses to their business customers’ needs.2 For example, Rolls-Royce plc competes by providing airlines with “Power By The Hour” — selling the jet engines along with the services to maintain, repair and upgrade them over many years. And providers of services such as IT, telecom network management and technical consultancy now compete by offering solutions that incorporate products from a few select manufacturers. Electronic Data Systems Corp., the global IT service provider, has built the capabilities to manage and integrate different suppliers’ technologies and products as part of its business outsourcing solutions.

The shift has been underway since the early 1990s. Looking just at the manufacturing side, a growing number of manufacturers have begun providing services to finance, operate, maintain and upgrade an installed base of products — their own and, increasingly, those of other manufacturers. Services are attractive because they provide continuous revenue streams, have higher profit margins and require fewer assets than manufacturing. By the late 1990s, revenues obtained by servicing an installed base represented from 10 to 30 times the value of new product sales.3 For example, Ericsson estimated in 2001 that the costs of purchasing a mobile communication network represented only 6% of the total costs of operating a network over a 10-year period. Across a range of manufacturing companies, service revenues now represent an average of over 25% of total revenues.4 For some, such as Rolls-Royce and IBM Corp., services that add value to the physical product now account for more than 50% of their revenues.5

But customers are not paying just for an integrated package of products and services. They are buying guaranteed solutions for trouble-free operations. The onus is on the providers of integrated solutions to identify and solve each customer’s business problem by providing services to design, integrate, operate and finance a product or system during its life cycle. In the United Kingdom, for example, the first integrated solutions contract for Alstom Transport (a division of Paris-based Alstom), awarded in 1995, was to renew the fleet of trains on the London Underground’s Northern Line. The contract did not simply specify the size of the fleet: It required that 96 trains be available for service each day. To achieve this target, Alstom built 106 trains and established a dedicated maintenance organization to service them.

Companies like Alstom are steadily building up the skills and competencies to become highly effective providers of integrated solutions. Pioneers of this business model, such as IBM, continue to modify their corporate strategies as their markets and their customers’ requirements evolve.6 But many other large companies are finding no shortage of obstacles to achieving growth and profitability in these new markets. They are realizing that traditional structures and capabilities have to be transformed and continuously refined. They have to re-evaluate their views of their customers. And they are learning that the new model is about systems integration and the provision of services.

Although there is a growing body of research on the challenges and opportunities of the integrated solutions business model, there is still very little that offers a blueprint for its implementation. As part of their studies of innovation in complex products and systems, the authors have examined the hallmarks of major providers and devised a framework that they believe can guide those trying to formulate effective integrated solutions strategies. (See “About the Research.”) This article highlights the importance of four prerequisite capabilities and examines the organizational structures necessary for success — structures that are reconfigurable around each customer’s needs and no longer bounded by product, service, brand or geographic lines. We then lay out three levels of organizational capability that describe the journey integrated solutions providers must take. Ideally, the resulting solutions will be “repeatable” —profitable and efficient enough to allow the experiences gleaned from initial projects to readily be applied to others.

Solutions for Integrated Systems and Services

Demand for integrated solutions is driven by the trend for large businesses to outsource systems integration and operational activities. Governments are also demanding far-reaching answers to their needs for major public projects — such as railways, hospitals and defense systems — which are designed, built, operated and financed by private companies.

Faced with declining profitability, slower growth and commoditization in their core product markets, many manufacturers are outsourcing an increasing proportion of their production activities and focusing on more profitable systems integration and service activities. For example, in the 1990s, manufacturers experienced a dramatic increase in the demand for turnkey projects, in which suppliers must design and integrate systems as well as provide services such as maintenance, leasing and financing. Alstom Transport is a case in point: In 1998, the railroad equipment company, which already had a systems-integration business, created a Service Business division as a result of a major strategic review that recognized the huge growth in the market for railroad rolling stock maintenance services. Today, Alstom outsources the production of almost 90% of the components incorporated in its train and signaling systems products.

The provision of integrated solutions is also attracting companies with a base in services.7 These companies are developing strong partnerships with product suppliers while strengthening their internal capabilities in systems integration. For example, WS Atkins plc, the consulting engineering and architecture group based in Surrey, United Kingdom, has developed the capabilities to integrate diverse suppliers’ technologies into systems that it can finance, operate and maintain for customers in transportation, defense, health care and other sectors.

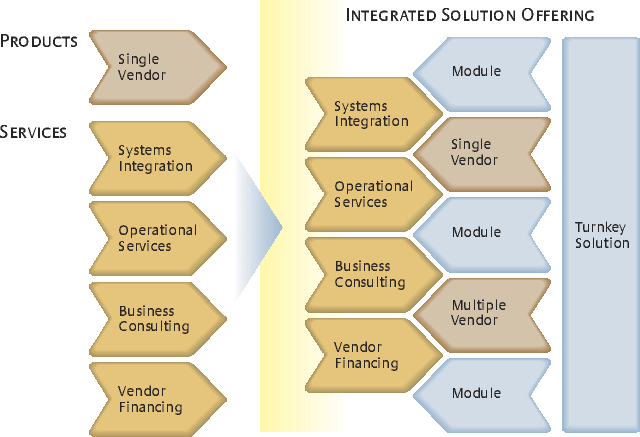

Regardless of whether the company came from manufacturing or service roots, each potential provider of integrated solutions must offer a wider range of discrete and bundled offerings than before. And each must understand that an ability to integrate systems is vital. In essence, systems integration is no longer a technical engineering-based task; it is a core strategic business activity to help customers use technology to create value and transform their businesses. (See “The Migration to Integrated Solutions.”)

Companies that plan to move into integrated solutions must have a clear understanding of what they do well and what new capabilities they need to develop. They must decide which capabilities can be provided in-house, which are no longer required and when partners are needed to fill capability gaps. In effect, they must be able to demonstrate four key capabilities: systems integration, operational services, business consultancy and financial services. (See “The Key Categories of Integrated Solutions Capabilities.”) Each deserves further scrutiny.

Systems Integration: Single Vendor or Multivendor?

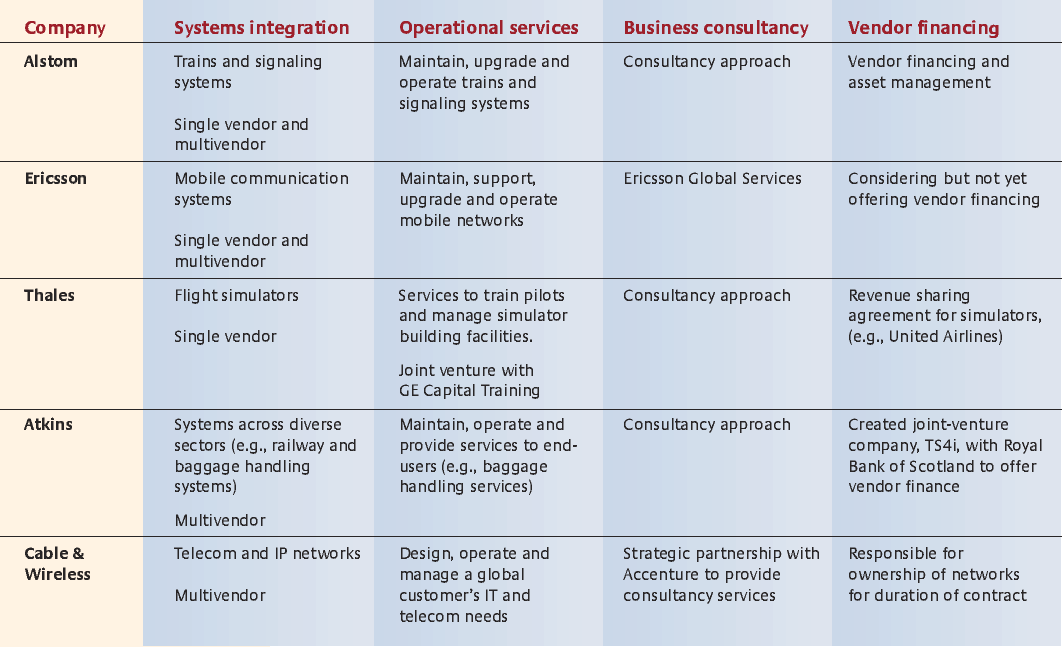

Systems integration is the core capability required to specify, design and integrate the physical components of a solution, including the hardware and embedded software that form a system such as a mobile communications network.8 Systems integrators outsource an increasing proportion of their production activities to external manufacturers, while retaining the capabilities to lead complex projects and manage large networks of suppliers and customers. At root, their job is to ensure that the value of the system to the customer is greater than the sum of its component parts. The challenge of creating value is accentuated by the increasing technological complexity of the systems. For example, Ericsson Inc. recently developed 3G mobile phone systems that had to be integrated into phone networks that were already fully operational, while working smoothly with the previous generation of circuit-switching technology.

Companies face a strategic choice about how to specify and integrate the physical components into a system. They can incorporate their internally developed technologies and products, as manufacturing-based companies such as Alstom and Ericsson have done (and continue to do) successfully. Or, like telecom solutions provider Cable & Wireless plc, they can utilize technologies and products from leading manufacturers. With no in-house production capabilities of their own, service-based companies often have a flexibility advantage, because they can select and tailor the best multivendor system to a customer’s needs. The Global Markets division of Cable & Wireless Global relied on strategic partnerships with equipment producers Nortel Networks Corp. and Cisco Systems Inc. to provide its customers with multivendor network solutions that Cable & Wireless designed, installed, operated and supported.

IBM was one of the first to recognize that the acid test is the ability to specify and integrate a competitor’s technology if a customer demands it or when it provides a superior solution. Companies such as Thales’ Training & Simulation Ltd. that remain tied to a single-vendor strategy have to be confident that their products can compete with multivendor approaches offering a choice of technologies and products.

Operational Services

Because systems integrators have an intimate understanding of their customers’ needs and the systems that have been designed, they are well placed to provide services to operate, maintain and upgrade a system during its operational life. Operational services include intangible services, such as maintenance, spare parts supply and training, and software-based services embedded in the physical product, such as fault reporting and remote diagnostic systems.

Involvement in operational services opens the door to future orders for new products, upgrades and replacement parts. Alstom’s service unit offers “Total TrainLife Management” services that include maintenance, renovation, spare parts and asset management. The typical life cycle of a train extends over 30 years: two years to design and build rolling stock and 28 years to provide services that continuously generate strong revenue streams.

As solutions providers gradually take over a customer’s operational activities, they have additional incentives to design systems from the start that are more reliable and more easily maintained. Alstom made 250 design modifications to ensure that the Northern Line Tube trains would be easy to use and simple to maintain. Similarly, with the right processes in place, lessons learned from operations can flow back into improved designs of new products.

Business Consultancy

Integrated solutions companies typically provide advice on how to identify, diagnose and solve operational and strategic problems, develop business plans, exploit the potential of complex new technologies (such as 3G mobile systems), select and link technology to improve a customer’s business processes and transform a customer’s traditional business model.

Companies are developing these capabilities by creating joint ventures with professional services companies acquiring consultancy companies or developing consultancy skills in-house. Cable & Wireless offers consultancy to corporate customers through its partnership with Accenture Ltd., while Ericsson and Atkins have developed their own consultancy organizations. Ericsson Global Services was established in 2000 to help provide customers with advice on their strategies for mobile communications, such as how to write business plans, finance and manage their assets, produce network designs and develop applications for 3G mobile services.

Vendor Financing

Some companies offer vendor financing. It may take the form of value-sharing contracts that lower the purchase price of a system in return for a proportion of the future value generated during its operational life, or it may constitute asset management to reduce the costs and extend the operating life of an installed base of products.

In the United Kingdom, many companies have developed such capabilities to meet a growing demand for large public projects that are designed, built, operated and financed by the private sector. However, few companies have been able to follow General Electric Capital Services Inc. by moving beyond financing in-house products into multivendor solutions. One way to do this is through strategic partnerships. In 2000, WS Atkins created Total Solutions for Industry, a joint venture with the Royal Bank of Scotland plc that gives customers a single source of integrated solutions for finance along with design, construction and maintenance services. Serving contracts with an asset value of between £5 million and £20 million (about $8.8 million to $35.4 million), the joint venture offers to manage assets for customers, such as mobile telephone base stations, baggage handling systems and power stations. The bank supplies the financing and specific financial services, such as equity savings, while Atkins handles design, construction management and asset management.

Rethinking the Organizational Structure

To achieve success in the business of integrated solutions, companies must build their organizations around their customers’ current and future needs. The reworked organizations must evolve so that they can provide tailored combinations of products and services that solve specific problems.

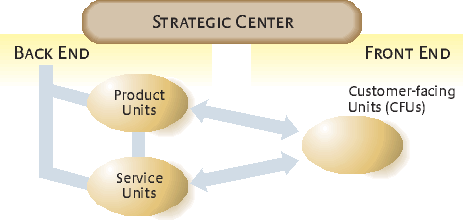

In a shift away from traditional structures, companies are creating new types of organizations that are reconfigurable around each customer’s needs. (See “A Three-Part Organizational Structure.”)9 These organizations comprise front-end customer-facing units, back-end capability providers and strong strategic centers.

Controlling Access to the Customer

To become a solutions integrator, a company must first gain control of the channel to market. Channel control is imperative because any attempts to move downstream toward the business customer will be blocked if another company controls the customer interface. Thales’ early attempts to move into the fast-growing market for flight simulation training solutions were thwarted by specialized training schools such as GE Commercial Aviation Training, which have taken on the additional training tasks now outsourced by some of the commercial airlines.

Of course, channel conflicts can be resolved by buying the channel. IBM acquired one of its competitors — PwC Consulting — so it could consolidate its control of global IT markets. Another option is to form partnerships with the channel controller, as Cable & Wireless has done.

Alstom and Ericsson have not faced such channel conflicts because they already have strong relationships with their customers. But they run into those conflicts if they move too aggressively into the customer’s territory — or move there without prior agreement. As long as customers see the value of integrated solutions and request them, there is no conflict; they consider such moves to be of mutual benefit, both strategically and in terms of short-term value creation.

Once channel control is established, companies must create customer-facing units to manage strategic engagements with the customer, develop value propositions, integrate systems and provide operational services. CFUs range from single projects to permanent business units set up to meet a customer’s ongoing needs. These groups must be multiskilled and cross-functional. They are comprised of key account managers, financial analysts, legal experts and a large number of staff with commercial, project management and technical design expertise. The CFU is organized so that the company’s back-end product and service capabilities and its network of external suppliers are channeled through the project implementation team at the point of contact with the customer.

The project teams, including members from the CFU, back-end capabilities providers and the customer’s organization, can be rapidly assembled, disbanded and reassembled around each customer’s business problem. For example, Ericsson’s customer-facing division, called Ericsson Vodafone, is located next to Vodafone’s U.K. headquarters and works on many collaborative project teams to develop and commercialize mobile technologies, products and applications.

Building Modular Offerings on the Back End

Back-end units provide common components of solutions-ready products and services that can be “mixed and matched” in different combinations by the CFUs. They can be in-house organizations or partners supplying the core product or service components of a solution. They are made up of staff with specialized expertise in areas such as product development, marketing, communications, human resources, professional services and systems integration.

Product units must develop common technology and standardized product platforms that can be easily configured to provide more efficient solutions for each customer’s needs. For instance, Ericsson’s 3G systems portfolio was developed to provide mobile operators with a range of products at low cost. Under this front/back structure, internal product units must learn to become flexible and responsive to the front-end demands for resources and capabilities.

Much the same applies to services offerings: They must be developed as modular units that are consistent, easy to understand and easy to assemble into customized solutions. In this way, the CFUs can select predeveloped service offerings from the portfolio rather than developing customized services for every new project. Ericsson estimates that up to 75% of the service component of its integrated solutions can be based on its off-the-shelf reusable modules. (The remaining 25% must be customized by the CFU at the point of contact with the customer.) The modular, reusable approach cuts costs and improves the reliability of the integrated solutions. Relying on standardized business processes, pricing and guarantees for service reliability, the service portfolio is constantly revised to improve the process of selling and delivering solutions.

Defining the Role of the Strategic Center

The strategic center must develop strategies, organizational structures and brand names to support the global delivery of integrated solutions. It is responsible for encouraging collaboration between front-back and internal-external capability providers. A strong corporate center is required to forge effective links between the front and back organizations to enable a speedy and rich flow of knowledge and information. CFUs must pass knowledge to the back-end units to assist in the ongoing development of “solutions-ready” components; the back-end units have to turn today’s customized solution into tomorrow’s standardized offering.

Essentially, the strategic center must adjudicate between the front-end pull of customization and the back-end push for standardization. Although the front-end CFUs are driven to meet their customers’ calls for innovative and unique solutions, too much emphasis on customization can impede the provision of repeatable solutions. But the pendulum cannot swing too far the other way: The strategic center must recognize the limits to standardization and replication. Some of the largest and most sophisticated business customers — such as mobile phone operators and airlines — can find that their needs are not fully satisfied by solutions comprised mainly of standardized modules.

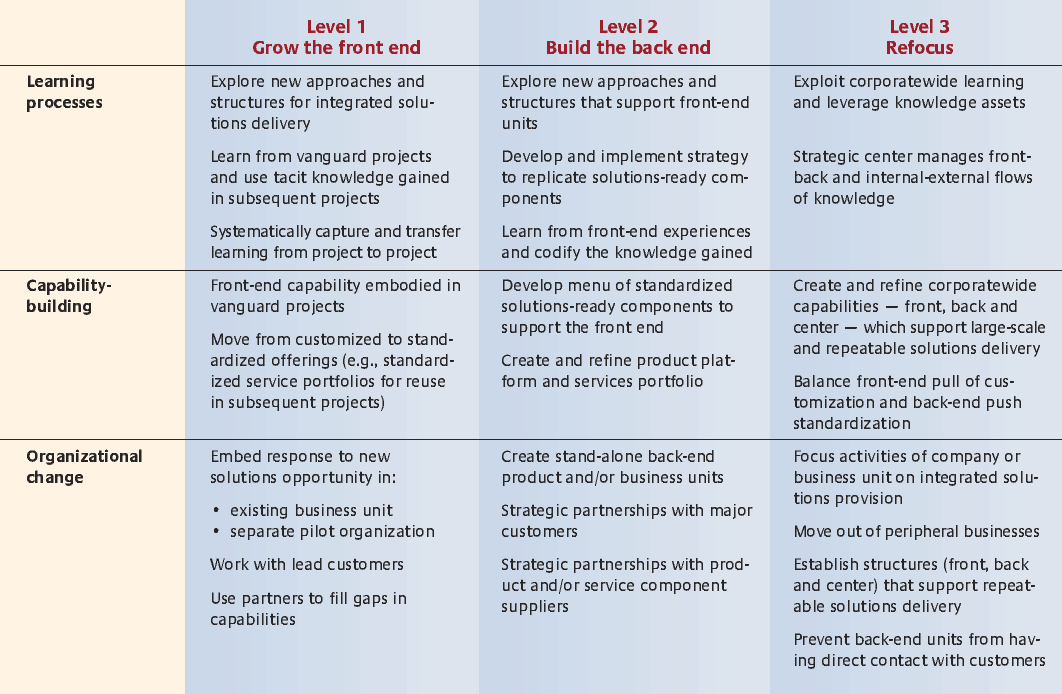

A Three-Phase Capability Model for Building Repeatable Solutions

So what is required to become a truly capable integrated solutions provider? It is necessary to move through three levels of organizational capability. At Level 1, the company must build a new face to the customer, at Level 2, it needs to strengthen its back-end capabilities and, at Level 3, the organization — front and back — must be refocused around customers’ needs and around repeatable, integrated solutions delivery.

As companies continue to learn from their experiences and work through the challenges of capability-building at each level, they can make deliberate strategic decisions to climb to the next level in the organizational capability model. (See “Organizing for Repeatable Solutions.”)

Repeatability is the measure of a company’s progress in providing integrated solutions.10 Initially, there is a powerful incentive for suppliers to offer customized solutions by creating tacit knowledge and new organizational approaches tailored to the context of each customer’s problem, since this capability distinguishes them from rivals. But offering expensive customized solutions for each new customer is not enough to guarantee long-term growth and profitability. The knowledge and experience gained from initial integrated solutions projects must be shared, codified into project manuals and business processes and reused in subsequent projects. The costs of developing initial solutions must be recovered by replicating the product and service components of solutions until they become standardized offerings, used repeatedly in many projects at lower costs.

Success in integrated solutions depends on how quickly and easily a company can move from unique to repeatable solutions delivery. It is about balancing customization and standardization. The balancing act begins the moment a company wins new projects and starts to scale up for repeatable solutions.

Level 1: Build a New Face to the Customer

The slow, costly process of capability building starts when a company carries out its vanguard projects for integrated solutions. IBM’s journey can be traced back to 1989, when it won a major outsourcing project to design, build and operate Eastman Kodak Co.’s data processing center. Cable & Wireless’ first move occurred in 1998, when it won a very large out-sourcing project to provide Accenture Ltd. of Bermuda with a global telecom and Internet protocol solution from a single source.

In this phase of front-end exploration, new approaches for integrated solutions are created and refined. The initial projects are incubated by embedding the new project in the existing business unit or setting up a separate pilot project organization.11

An example of each: By embedding its integrated solutions capability within its existing product offerings, Thales was able to incrementally enhance its capabilities for integrated solutions. By establishing pilot projects, Ericsson, Alstom and Cable & Wireless minimized the risk of initial moves while remaining free to experiment with new capabilities and approaches.

To meet growing demand for integrated solutions, initial project organizations have to increase the size and range of their capabilities. An effective strategy is to focus initially on developing solutions for lead customers that can be adapted and replicated for future customers at far lower expense. To reduce the risks of failure and the costs of repeating mistakes, successful lessons learned from initial projects must be systematically captured and transferred to subsequent projects. In that way, initial projects can grow into larger programs and ultimately into stand-alone CFU organizations. Because the type of customer and size of the market can vary widely, different types of CFU project organizations must be created: industry-based segments, customer groups within an industry, single customers and single projects.

Alstom Transport has set up two customer-facing divisions. Alstom Systems undertakes major systems integration projects to provide turnkey solutions for trains, signaling systems and maintenance services. Alstom Services offers operational services, such as train maintenance, technical support, product upgrades and renovation. Alstom has used the single-project organization model as part of its West Coast Main Line contract to design, build and maintain 53 high-speed tilting trains for London’s Virgin Rail Group. The work included the establishment of a special-purpose company, West Coast Traincare Ltd., to maintain the trains.

Level 2: Strengthen the Back-End Capabilities

Companies that win a large number of integrated solutions contracts must be able to field the modular products and services that can support their CFUs. So, a second capability step starts when a company begins to experiment with organizational structures and to develop new ways of utilizing corporatewide knowledge assets and resources.

Replication of product and service components presents a different set of challenges depending on whether a company started out from a base in manufacturing or in services. Service companies like Atkins have focused on developing product platforms in strategic partnerships with system manufacturers. Product companies encounter different organizational challenges. In the mid-1990s, companies such as Alstom had in-house product units but no obvious capabilities in services. Often it was the product units that led the way by setting up a variety of service organizations to tap into these unexploited sources of revenue. However, these sporadic moves led to a proliferation of inefficient and often redundant services. To better coordinate these activities, Alstom, like others, made the strategic decision to create a stand-alone service organization.

Ericsson Global Services is responsible for developing a global service portfolio that can be used by the company’s customer and marketing units. By 2003, the 250 disparate service offerings previously developed by its product divisions had been consolidated into a simplified, standard service portfolio consisting of three service families called Advise, Integrate and Manage. The portfolio addresses each mobile operator’s life cycle needs for advice in areas such as initial business ideas and planning, systems integration and management of network operations. Depending on their needs, customers can select an individual service module or a full turnkey solution for services and products.

Managers of back-end units must adjust to a new role in their organizations by learning to treat CFUs as both the internal customer and the distribution channel. They must get used to striking bargains and compromises over internal margins with CFU managers. Ultimately, they must hand over control of key customer accounts to the CFUs. It is anything but easy, as Cable & Wireless’ experiences show. (See “Cable & Wireless’ Tough Decision.”)

Level 3: Refocus the Organization

A company that believes it is ready to move to the third level must have experienced sufficient demand to warrant refocusing the entire company — or the relevant business division — on integrated solutions. In this exploitation phase, the challenge is to create and refine the capabilities of the entire organization — front, back and center — to enable large-scale, repeatable delivery of integrated solutions.

The corporate management team now must make a decision to channel the company’s capabilities to the customer through a single point of contact — the CFU. The executives must reorganize product and service capabilities into back-end organizations and realign the role and responsibility of the strategic center. When companies create the CFUs with sole responsibility for channels to market and customer relationships, they often face strong resistance from the in-house product or service units. Traditional business units often see the moves as threats to their power base and status. They may be reluctant to cede control of their accounts, and they may be downright resistant to the idea that the CFUs will propose solutions that incorporate a competitor’s technology or products — as happened at IBM prior to the creation of its IBM Global Services unit in 1996. Unless a strong center can successfully manage the interfaces between the newly formed front and back units, the units may pursue diverging strategies, becoming deadlocked over priorities and constantly swapping accountability for success and failure. It’s the job of the strategic center to resolve such conflicts and overcome resistance to the new structure.

Successfully refocused organizations are able to balance customization and standardization. They understand that the integrated solutions offering has to differ according to the needs, sophistication and product life cycle requirements of their customers. Less experienced customers often require more standardized solutions throughout the product life cycle. Because of the complexity of the problems they face, more sophisticated customers can find their needs are not fully satisfied by more standardized solutions. They may require help only at earlier stages, such as product introduction, rather than at large-scale rollout. For example, Ericsson has worked closely with lead customers such as Vodafone to create highly customized solutions for commercializing the new generation of 3G mobile system technology.

The trend toward more complex integrated solutions projects has been driven by the incorporation of new technologies and multivendor approaches that have expanded the number and range of physical components and services that have to be integrated. Companies that rise to the challenge of creating feasible and low-cost solutions out of this complexity can add substantial value for their customers. Early movers in integrated solutions are finding a vital source of competitive advantage in their growing ability to rapidly convert the learning gained on previous projects into reusable components that can simplify the process of integration.

Overcoming Challenges

The challenges of moving into integrated solutions should not be underestimated. To be able to develop a profitable business, prospective integrated solutions providers must overcome several obstacles to change. Traditional in-house product or service businesses must be persuaded to specify and sell solutions incorporating multivendor products and must learn to view the CFU as a valid channel for internally developed products and services. Changing the mindsets of thousands of employees who have grown up with a narrow vision of traditional products or services is perhaps the biggest barrier of all.

There is no single best way to become a solutions integrator —and there is no guarantee of success. The authors freely acknowledge that the transformation required is a formidable undertaking. A company can leap ahead to a more advanced level, develop its capabilities in parallel along two or more levels, stay where it is or even revert to a previous level if the strategy fails or the market for integrated solutions does not take off.

The recent misfortunes of some companies that have moved into integrated solutions raise questions about whether the journey is appropriate for all businesses. But this does not mean that companies should not set out on the journey. For example, despite the initial success of its 1995 Northern Line project, Alstom’s recent failure to achieve its customer’s targets for train availability and reliability led to calls in 2005 to end Alstom’s 20-year contract. What the critics didn’t see was Alstom’s success with another project to supply and maintain the Tube’s Jubilee Line. If the critics had known that information, they would have seen how the company had learned from its initial experiences and improved its capabilities.

Some companies have been able to move systematically through the three levels of capability. (See “Ericsson’s Story.”) Ericsson has found that Level 3 is not necessarily characterized by organizational stability. Like IBM, it continues to experiment with different organizational approaches and engage in new types of partnerships with suppliers and customers in response to new business opportunities.

For many companies, the challenges of building an integrated solutions business may seem altogether too complex and too committing at this time. But it is a journey that they must begin soon. Customers and markets are pushing them in that direction. And shareholders will soon do so too as they begin to understand how an integrated solutions model can enhance profitability and strengthen business continuity. The authors believe that before long, the locus of competition will have changed. The new market leaders will be those that have followed a clear road map to success in integrated solutions.

References

1. The trend toward solutions was foreseen by P.F. Drucker, “Innovation and Entrepreneurship: Practice and Principles” (London: Heinemann, 1985), 231. For a discussion of the emergence of customer solutions business models in the 1990s, see A.J. Slywotzky and D.J. Morrison, “The Profit Zone: How Strategic Business Design Will Lead You to Tomorrow’s Profits” (Chichester: John Wiley & Sons, 1998); and A.C. Hax and D.L. Wilde II, “The Delta Model: Adaptive Management for a Changing World,” MIT Sloan Management Review 40, no. 2 (winter 1999): 11–28. For a discussion of consulting capabilities required for customer solutions provision, see R. Sandberg and A. Werr, “The Three Challenges of Corporate Consulting,” MIT Sloan Management Review 44, no. 3, (spring 2003): 59–66.

2. Integrated solutions is one of several service-based business models; see R. Wise and P. Baumgartner, “Go Downstream: The New Profit Imperative in Manufacturing,” Harvard Business Review (September–October 1999): 133–141; and R. Oliva and R. Kallenberg, “Managing the Transition from Products to Services,” International Journal of Service Industry Management 14, no. 2 (2003): 160–172. However, previous research is limited to individual cases of companies or specific industries and neglects to identify the role of systems integration and the range of service capabilities required for integrated solutions provision. For a systematic empirical study showing how companies across industries are building specific capabilities for integrated solutions, see A. Davies, P. Tang, T. Brady, M. Hobday, H. Rush and D. Gann, “Integrated Solutions: The New Economy between Manufacturing and Services” (Brighton: SPRU-CENTRIM, 2001), 1–43.

3. Wise and Baumgartner, “Go Downstream,” 134.

4. See P. Koudal, “The Service Revolution in Global Manufacturing Industries” (New York: Deloitte Research, 2006).

5. For a discussion of services added to the physical product, see J.B. Quinn, “Intelligent Enterprise: A Knowledge and Service Based Paradigm for Industry” (New York: The Free Press, 1992); and M. Sawhney, S. Balasubramanian and V.V. Krishnan, “Creating Growth with Services,” MIT Sloan Management Review 45, no. 2 (winter 2004): 34–43.

6. For a firsthand account of IBM’s move into integrated solutions, see L.V. Gerstner, Jr., “Who Says Elephants Can’t Dance? Inside IBM’s Historic Turnaround” (New York: Harper Collins Publishers, 2002).

7. Several authors assume that the shift toward integrated solutions can be understood as a movement downstream from manufacturing to services, including Wise and Baumgartner, ”Go Downstream” and Oliva and Kallenberg, “Managing the Transition from Products to Services.” However, cross-sectoral research has found that companies are also moving into integrated solutions from a base in services. See A. Davies, “Moving Base into High-value Integrated Solutions: A Value Stream Approach,” Industrial and Corporate Change 13, no. 5 (2004): 727–756; and A. Davies and M. Hobday, “The Business of Projects: Managing Innovation in Complex Products and Systems” (Cambridge U.K.: Cambridge University Press, 2005).

8. For an in-depth discussion of systems integration, see M. Hobday, A. Davies and A. Prencipe, “Systems Integration: A Core Capability of the Modern Corporation,” Industrial and Corporate Change 14, no. 6 (2005): 1109–1143.

9. An organizational model for solutions is developed by several authors: See N.W. Foote, J.R. Galbraith, Q. Hope and D. Miller, “Making Solutions the Answer,” McKinsey Quarterly (2001): 84–93; J.R. Galbraith, “Organizing to Deliver Solutions,” Organizational Dynamics 31, no. 2 (May 2002): 194–207; and J.R. Galbraith, “Designing Organizations: An Executive Guide to Strategy, Structure, and Process” (San Francisco: Jossey-Bass, Wiley, 2001). However, these authors assume that back-end units are in-house because their research is based on vertically integrated manufacturing companies like IBM, Nokia and Sun Microsystems. For a model that recognizes that integrated solutions providers can originate from services and that back-end units can be external to the company, see A. Davies, T. Brady and P. Tang, “Delivering Integrated Solutions” (Brighton: SPRU-CENTRIM, 2003): 1–34.

10. For a discussion of repeatable solutions, see A. Davies and T. Brady, “Organizational Capabilities and Learning in Complex Product Systems: Towards Repeatable Solutions,” Research Policy 29, (2000): 931–53; Galbraith, “Organizing to Deliver Solutions”; and T. Brady and A. Davies, “Building Project Capabilities: From Exploratory to Exploitative Learning,” Organization Studies 25 (2004): 1601–1621. The concept of replication is discussed by S.G. Winter and G. Szulanski, “Replication as Strategy,” Organization Science 12, no. 6 (2001): 730–743.

11. E. Cornet, R. Katz, R. Molloy, J. Schädler, D. Sharma and A. Tipping, “Customer Solutions: From Pilots to Profits” (Boston, Massachusetts: Booz Allen & Hamilton, 2000), 1–15.