Brand Management Prognostications

Topics

The use of brands has been central to marketing for more than a century. The dominant logic has been “Build a brand, and the world will beat a path to its door.” Long-standing brands such as Marlboro, Coca-Cola, Xerox, IBM, and Intel are considered to be among the world’s most valuable assets. This precedent spurs diverse firms to base their strategies almost entirely on building brands. Car manufacturers, insurance companies, banks, and even industrial chemical producers are structuring themselves along brand and product lines, making brand managers responsible for the success of single brands or categories of products.1

Recently, many have questioned the wisdom of the brand management approach and the value of brands.2 In this article, we address the following issues:

- What is the point of marketing without brands?

- If brand managers are no longer responsible for brands, who is responsible?

- Is the brand-manager concept dead or merely ailing?

- Will brand management rise again, phoenix-like, in modified form?

We begin with the simple question: “What does a brand do?” That is, which functions do brands perform for the participants in a marketing relationship? We then identify the pressures that are influencing the evolution of brands and brand management and are leading to reappraisal of the brand-manager system. Finally, we identify three possible scenarios for brand management and their implications for firms that adopt them. We argue that only by focusing on the customer-oriented functions that brands fulfill3 can we gain some insight into the changes that may affect the evolution of both brands and brand management. Although we offer no definitive master plan for confronting the challenges posed by the demise of the brand manager, we find that common uncertainties must be alleviated, irrespective of the evolving organizational models.

Functions of a Brand

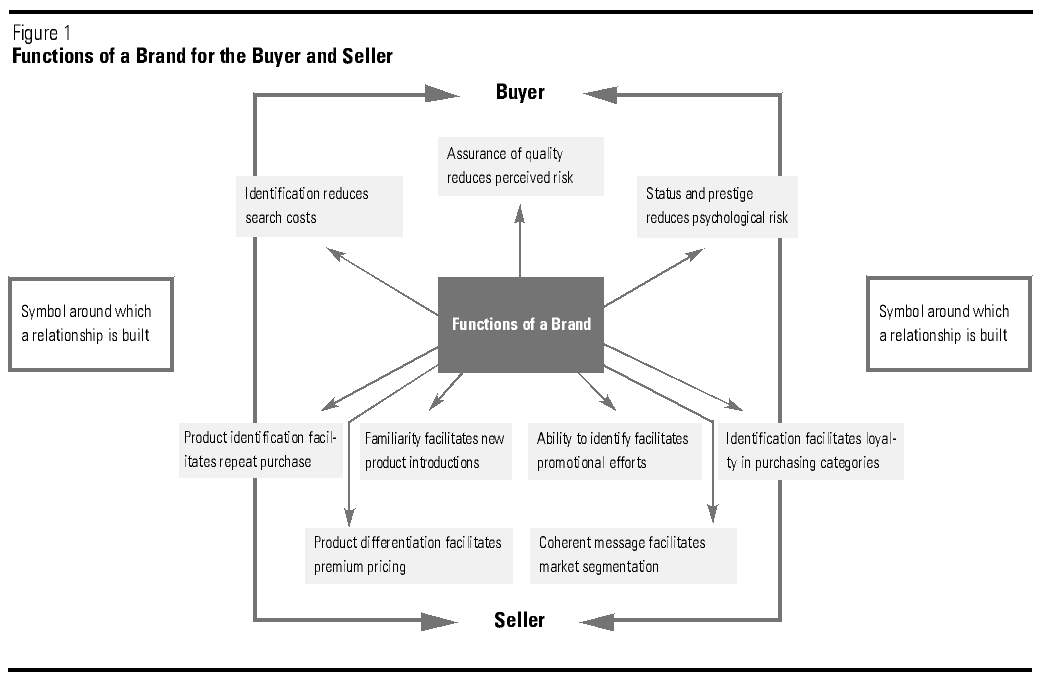

The quintessential function of branding is to create a distinction among entities that may satisfy a customer’s need. This primary distinction is the origin of a series of benefits for both the buyer and the seller4 (see Figure 1).

{kind=link}

For buyers, brands effectively perform the function of reduction: brands help buyers identify specific products, thereby reducing search costs and assuring a buyer of a level of quality that subsequently may extend to new products. This reduces the buyer’s perceived risk of purchasing the product. In addition, the buyer receives certain psychological rewards by purchasing brands that symbolize status and prestige, thereby reducing the social and psychological risks associated with owning and using the “wrong” product.

For sellers, brands perform the function of facilitation — that is, they ease some of the seller’s tasks. Because brands enable the customer to identify and reidentify products — all things being equal, this should facilitate repeat purchases on which the seller relies to enhance corporate financial performance. Brands also facilitate the introduction of new products. If existing products carry familiar brands, customers will generally be more willing to try a new, seemingly appropriate product if it carries the same familiar brand. Brands facilitate promotional efforts by giving the firm something to identify and a name on which to focus. Brands facilitate premium pricing by creating a basic level of differentiation that should prevent the product from becoming a commodity. Brands facilitate market segmentation by enabling the marketer to communicate a coherent message to a target customer group — effectively conveying for whom the brand is intended and, just as importantly, for whom it is not intended. Finally, brands facilitate brand loyalty, particularly important in product categories in which repeated purchasing is a feature of buying behavior. (We argue that this is a facilitative function distinct from that of identification, which permits ease of repurchase for the buyer but does not ensure it.)

Brands appear to fulfill more functions for sellers than for buyers (see Figure 1), although a simple accounting does not reflect the inherent value of the functions to each party. However, this apparent imbalance underlines the infrequently acknowledged distinction between customer-based equity5 and organizational (or seller) equity.

Overall, brands have brought buyers and sellers together by serving as symbols around which both parties can establish a relationship, thereby creating a focus of identity.6 However, pressures to change branding and the brand management system —despite their venerable roles in business — are rising, as we now explore.

Pressures for Change

Brand management is generally believed to have emerged in 1931 when the president of Procter & Gamble decided that “each P&G brand should have its own brand assistants and managers dedicated to the advertising and other marketing activities for the brand.”7 Conceptually, the structure is pleasing in its relative simplicity. Creating a manager with overall obligation for a product or a brand is akin to giving an individual the responsibility and accountability for running his or her own business.8 Historically, these managers competed externally in the marketplace against competing brands (and frequently against other brands of the same company) and internally for limited corporate resources. Their brand’s marketplace success determined their own viability, just as it would in the case of an entrepreneur in charge of a business. Management bases financial rewards on the brand’s successful performance, normally assessed by monitoring shifts in the brand’s share of the market and/or its contribution to profit.

In recent years, however, new forces have caused major shifts in the brand-manager system, resulting in ruthless questioning of the value of brands as well as criticism of the brand-manager system. A Booz Allen & Hamilton study concluded that in the United Kingdom too many brand managers “were still sitting in their ivory towers failing to come to grips with the commercial realities of the job,” blaming methods of management for the situation.9 The popular business press has reported on radical changes in the brand-manager system in the firms where it originated, such as P&G and Unilever.10 Consulting firm BCG also has reported that 90 percent of U.S. consumer goods firms surveyed had restructured their marketing departments.11 Some suggest the emphasis of brands is merely shifting from the product-level brand to the corporate, “meta-level” brands that appear to be prospering (i.e., Coke, Microsoft, Disney).12

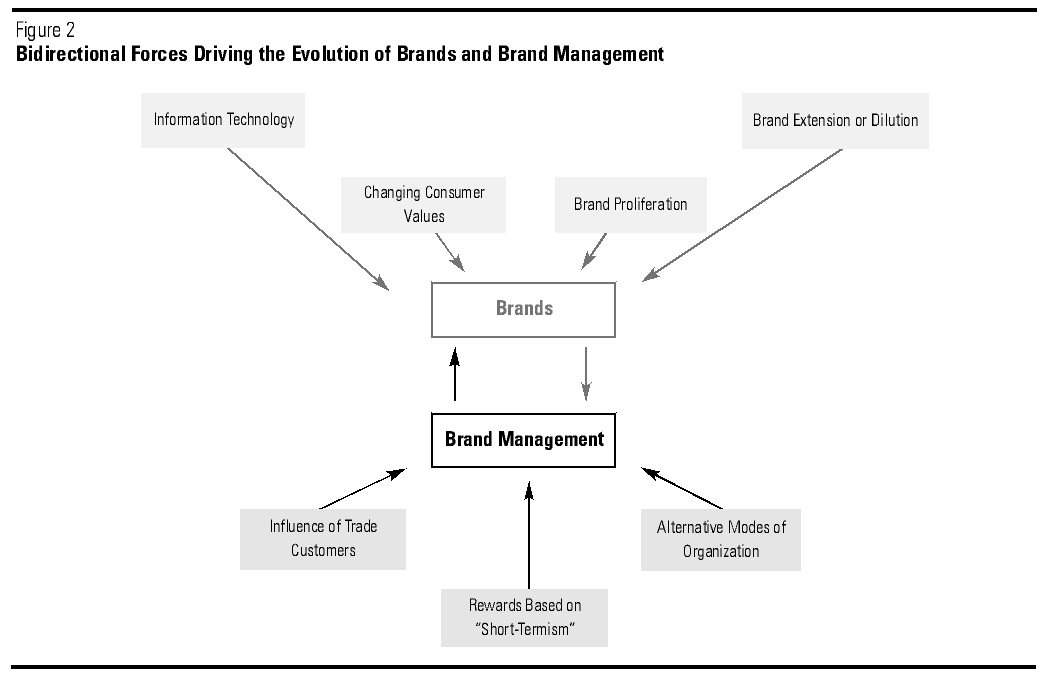

Next, we identify and expand on the bidirectional pressures for change affecting brands and the brand management system, as identified by Shocker et al.13 (Figure 2 represents these forces as systematic processes.)

{kind=link}

Influx of Information Technology

The adoption of information technology (IT) is shifting the power away from brand managers and will increasingly affect the role of the brand in simplifying customer search. IT enables more sophisticated stock control and merchandising among the better managed trade customers. IT implementations are permitting leading-edge retailers in the United States, Europe, and other parts of the world to develop consumer loyalty programs; ownership of this customer information is becoming the key to power.14 In the past, consumer goods manufacturers used market-research survey data about consumers to gain an informational advantage over trade customers. Today, major retail chains own real-time information (collected by scanners, massaged by sophisticated software, and linked to frequent shopper programs) that identifies individual shoppers. It is now the retailer who dictates whether a product will be given shelf space: in the United States, the fast-moving consumer goods marketer was paying up to $222 by 1990 to introduce a single new product into a single store.15 This shift in the distribution of power is not immutable, however. By using IT astutely, manufacturers can recapture power from the channel, and some are pursuing this course.16

The growth of direct marketing via catalog, telephone, television, and the Internet with its multi-media platform, the World Wide Web,17 is viewed as advantageous by many marketers. Ironically, this may turn out to be a marketing nightmare from a consumer-search perspective.

For the consumer, the Internet has the potential to substantially lower the cost of searching for information on products and services, which in turn will cause markets to become more efficient.18 Although Levitt19 argues that marketing is indispensable in commodity markets, there is no doubt that marketing works best and most effectively when the market is less than efficient. As markets approach efficiency, marketing in the traditional brand-oriented sense becomes increasingly problematic. Thus, two traders on a stock or commodity exchange floor can hardly be said to “market” to each other when they make a trade at a known price.20

The Internet may “commoditize” information, making customer search easier and less costly.21 Today, by using search engines, a buyer may seek, via the Web, a certain product with a set of desired features at a given price. In the future, via the Web, individual consumers may invite product suppliers to make their lowest electronic bids in order to win their business! Recent software developments include “intelligent agents,” which some experts predict will handle electronic errands and possibly make routine decisions for consumers; agents will monitor and learn from a user’s actions, make suggestions, and “even undertake the consumer’s handling in the marketplace.”22 For example, Bargain Finder is an intelligent agent that allows users to compare the prices of eight online compact-disc retailers. According to the Financial Times: “It addresses what is perhaps the thorniest issue surrounding the use of intelligent agents in electronic commerce — pricing. . . . Suppliers are anxious that they could lose business as customers use the Internet to compare prices. . . . It is a ‘totally painless way of letting the fingers do the walking.’ ”23

As IT developments make markets more efficient and possibly lessen the role of the search-cost-reduction function of manufacturers’ brands, the relevance and usefulness of the search agent or information provider’s brand are likely to increase.24

Changing Consumer Values

Changing demographics ensure that an ever-growing proportion of future markets will be composed of experienced buyers who are more self-assured, more willing to accept responsibility for judging the relationship between quality and price, more skeptical of superficial blandishments, and more capable of choosing from among a multitude of sellers. Much better attuned to what value is, they will seek it out tenaciously, aided in their search by technology.

What does this mean for marketers? Will it make strong brands even stronger or will consumers turn increasingly to house (retail) brands in their search for value (and the less obvious functions that brands perform for them)? Could the corporate brand become as important for products as it is for services (i.e., will shoppers seek to buy “baskets” of products from a reputable company — whether retailer or manufacturer)?25

Have brand managers been impervious to the slow but persistent fundamental change in consumer values? Namely, that the consumer in the late 1990s is far more value-conscious than in the 1980s?26 As Chanil put it: “More and more price-conscious consumers are demanding the best value in merchandise.”27 If a buyer’s peers also are seeking value, brands may become less relevant sociopsychologically. Furthermore, social status may be less a function of a person’s possessions in the twenty-first century than it has been in the last part of the twentieth century.

Let’s examine the phenomenon of changing values theoretically and practically. Dickson suggests that, in times of oversupply, consumers have greater choice and become more sophisticated.28 Marketers’ attempts to serve these more sophisticated consumers spur them to innovate, which, in turn, leads to imitation and again to oversupply. From a practical perspective, we know that the consumer population in the industrialized countries is aging and that older consumers learn from experience to be more discerning in their purchasing and consumption. Furthermore, in recent times, firms offer more services and higher product quality — that is, more value for the same amount of money. Consumers increasingly expect and even demand these added benefits. Assiduous consumer judgments of perceived quality versus price compel brand owners to accurately benchmark competitive value and price.

Brand Proliferation

In some markets, mimicry of brands has surfaced as producers attempt to survive through imitation. Successful pioneering brands attract competitors who introduce a plethora of competing brands that contribute little value or threat to the marketplace but add “noise.” Consumers, already bombarded by thousands of marketing messages daily, find their search costs increasing and their ability to differentiate between brands atrophying. This process leads to an overall degeneration of the brand as a marketing tool.

Brand Extension or Dilution

An accepted way to expand product range and volume is the extension of brands by introducing new products that leverage the brand across categories. Indeed, by the late 1980s, more than 80 percent of new product introductions in the United States were various extensions.29 However, brand extension, a rational strategy if well conceived and pursued with restraint, can all too easily degenerate into brand dilution. The lure of short-term volume gain through extension can “kill” or greatly weaken the parent brand — indeed, recent evidence seems to suggest that companies have begun to learn this lesson. A recent article inquired: “Does the world really need thirty-one varieties of Head & Shoulders shampoo? Or fifty-two versions of Crest?” The same article pointed out that P&G had begun cutting back severely on brand extensions in an effort to “make it simple.”30

Influence of Trade Customers

During the past twenty years, trade concentration has increased, as exemplified by supermarket retailing.31 Advancing more quickly in certain countries, trade concentration appears to be a global trend.32 In a survey of the United Kingdom’s top 500 advertisers, 54 percent of respondents agree that the “center of marketing gravity” has shifted to retailers. In reaction, some manufacturers are promoting categories, not brands — and retail power is a major factor behind this shake-up.33

Empowered by their increased market and information clout, retailers are in a position to manage for category profitability and to insist that both new brands and extensions augment total category profitability. This makes traditional zero-sum competition for shelf space among manufacturers less feasible. In the United States, many manufacturers have an opportunity to influence retail space planning (and, in some cases, act as subcontracted category managers for the retail trade), whereas, in Europe, retailers have have more typically performed those tasks themselves, often restricting and charging for access to shelves.

The short-term impact of this change on brand management has been considerable. Traditionally consumer-focused brand managers are now more cognizant of the importance of the trade customer and often work in category teams incorporating sales, logistics, finance, and other functions. More stringent criteria for shelf access, in turn, increase the pressure for packaging innovation and reduce opportunities for minor extensions and restagings. Many of these activities do not contribute to the economic profit (that is, shareholder value) of either the manufacturer or retailer. In some companies, this shift to category teams results in a new division of marketing responsibility: trade marketing managers or the sales function take responsibility for trade promotion (sometimes called operational marketing), while brand managers focus on target markets, brand development, and innovation. Category management permits manufacturers to avoid the worst excesses of internal competition, which has sometimes trammeled the traditional brand management system.

“Short-Termism” and Rewards

For companies capitalized and traded on the world’s major stock exchanges, ignoring shareholder value is a perilous course. To pursue short-term profit at the expense of long-term profit does not typically serve the interests of shareholders and can result in brand-destroying strategies. When reporting on the results of company operations, accounting conventions in most countries require the reporting of a balance sheet and an income statement. Clearly, to protect their interests, shareholders must know whether reported profits are associated with an increase or deterioration in net asset value. The ideal objective is to increase both profit and net asset value rather than trade off one against the other. In contrast, measurement and reward systems for brand managers do not make such distinctions. Typically, brand managers have been encouraged to improve short-term performance measures, such as operating profit or brand share, with little consideration of the consequences for the net asset value of the brand. Better managed, fast-moving consumer goods companies have recognized this problem and have incorporated into their assessment systems some kind of brand-equity measurement.34

Alternative Ways to Organize

Other approaches to the organization of marketing (other than brand or product management) include:

- A functional approach, whereby marketing is split into specialized functions, such as research, sales, and advertising, and individuals with particular skills in these areas are responsible for them.

- A geographic segment approach, whereby marketing is organized by regions, recognizing that different regions require different marketing acumen.

- A market or market-segment approach, whereby marketing is organized according to different target markets, and managers are responsible for each. Industry or end-use organization is particularly favored by business-to-business marketers. Thus a computer company might divide its market and assign managerial responsibility on the basis of various applications, such as banking and financial services, manufacturing, transport services, or retailing.

- A business process approach, which developed during the reengineering wave of the past few years, with cross-functional teams responsible for major activities.35

Sometimes used to streamline firms for optimal efficiency, these organizational arrangements may and often do coexist with some form of brand or product management, which impinges on the traditional primacy of the brand management structure.

Possible Future Scenarios

Changes in brands and the brand management systems are inevitable, especially with regard to the functions that brands perform for buyers and sellers engaged in a marketing relationship. For brand management, a variety of possible scenarios may emerge, and we explore these next.

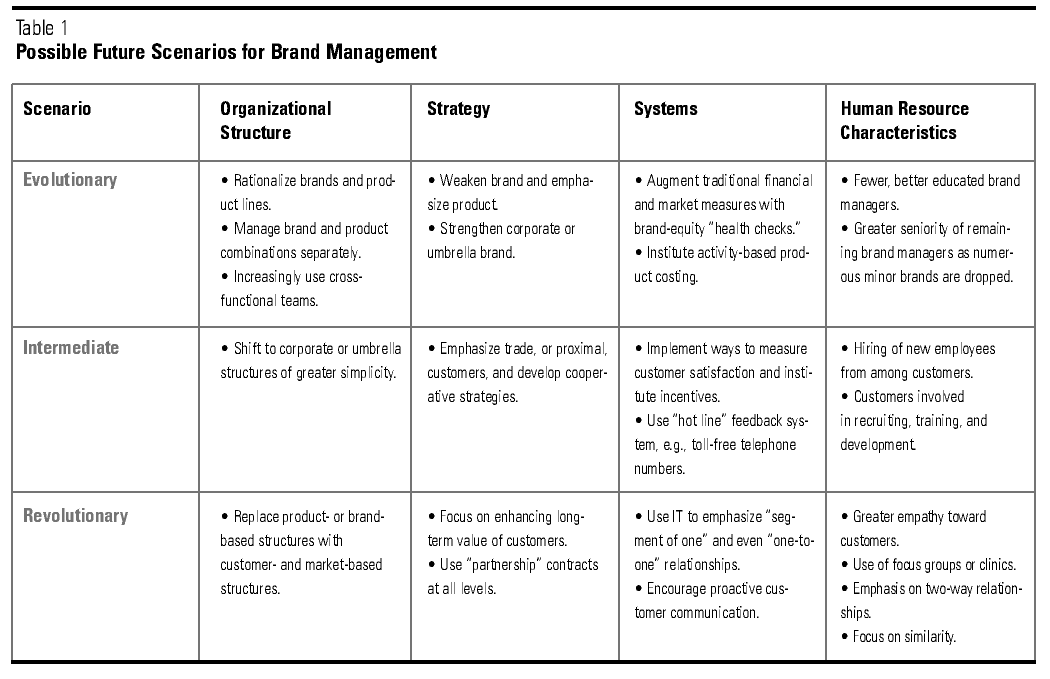

As discussed above, a brand or product-manager system is one of many ways to organize marketing. Indeed, many aspects of marketing do not need to be organized as specialist functions. If viewed as a general management function, marketing is the job of everyone within the organization, a philosophy that has much in common with total quality management.36 Although each method of organization has its advantages and limitations, brand management has been unusually resilient. Yet the idea of a brand manager and the managing of brands differ substantially. In this section, we focus on brand management per se, presenting three possible scenarios for the future — for simplicity referred to as the evolutionary, the intermediate, and the revolutionary (see Table 1 for a summary).

{kind=link}

Evolutionary Scenario

An evolutionary scenario is characterized by a continuation of current trends. As markets become more competitive and trade customers more assertive, the number of “me-too” brands and stock-keeping units will diminish. Its growth linked to affluence and two-worker households, convenience-store retailing will accentuate the pressure on many “other than leading” brands because of its restricted shelf space. Supermarkets seeking growth by adding new categories will increasingly have to weed out those manufacturers’ brands with less market share in traditional categories. As companies sort out their brand systems and ranges, we expect less emphasis on product-level branding and more on umbrella branding at the corporate and product family levels.37 In addition, the issues of brand architecture will become more prominent. On the basis of lessons learned from consumer goods marketers, we believe that the roles of product-level branding and corporate-level branding will be reversed in the future! Indeed, service firms have long recognized the cardinal position of the corporate brand.38

These changes will thin the ranks of brand managers, leaving a residual of senior-level personnel. Those who remain, however, will increasingly work in cross-functional teams, organized around categories and/or processes — a distinct change from the traditional model of brand management. Furthermore, we expect more companies to follow the lead of firms such as Nestlé in consciously elevating the hierarchical level of responsibility for brand-equity guardianship. Traditional financial and market measures of performance will be augmented by brand equity–based measures, and these will be more relevant in the evaluation process. As retailers propel direct product profitability and category management to more sophisticated levels, so will manufacturers seek ever improved methods of product costing, using tools such as activity-based costing. The shareholder value philosophy will penetrate further into the organization, and more brands and decisions will be reviewed for economic rather than accounting profit.39

Dealing with these changes will demand a better educated and more well-rounded cadre of brand managers than is currently employed by many firms. Indeed, if the prognosis of one marketing scholar is correct, future brand and marketing managers will need both the skills of an analyst and the financial aptitude of an investment banker, not to mention the interpersonal sensitivity of a skilled diplomat!40

Intermediate Scenario

The intermediate scenario is at least partially in place in some companies. Simplified brand and organizational structures will become strongly focused on trade, or proximal, customers — that is, retail chains in the industrialized countries and emerging large wholesalers in some less developed markets. Manufacturers will increasingly develop joint strategies with these proximal trade customers, although approaches will vary in different parts of the globe. In the United States, more retailers may follow K mart-like examples of subcontracting category management or even jointly developing store-based micromarketing strategies, as advocated by Kraft General Foods. In Europe, such proximal relationships tend to be more difficult, and the large French retailers, in particular, tend to resist this level of cooperation. Focus on proximal customers in the distribution system, however, will lead to considerable advances in efficient-consumer-response initiatives, as well as improvements in delivery and assortment performance and more sophisticated attempts to measure trade-customer satisfaction.

As part of becoming more customer-focused, we can expect significant changes in human resource management. Manufacturers will follow the example of service providers such as Southwest Airlines in coopting customers (via frequent flyer programs) to assist them in recruiting, screening, and selection procedures.41 More companies will involve customers directly in training and development activity, not only as speakers but as participants. Hiring from the firm’s customer base will be seen as another way to instill customer thinking into the organization, even though the impact of any one hire will dissipate over time. Some companies are beginning experiments with temporary job swapping between supplier and customer. Certainly, multilevel, multifunctional contact with the customer is likely to become the norm. Unfortunately, in the enthusiasm to embrace the proximal customer, the consumer receives less focused attention.

The value of consumer or end-user input to many marketing decisions is reflected in the recent novel approaches to marketing research. Such insight is also invaluable in helping to offset emergent intermediary power and should definitely be part of the marketer’s inventory of tools. Another tactic is the toll-free telephone number that is widely used on U.S. packaged goods and long treasured as a consumer resource by Japanese companies like Kao. The use of toll-free numbers is still quite rare in Europe and other parts of the world.

Revolutionary Scenario

The revolutionary scenario requires a radical rethinking of the roles of brands and customers in the management equation. As discussed earlier, brands influence buying behavior through the functions they perform for the customer. During their daily activities, customers process a vast amount of information and develop efficient ways of dealing with information overload. Heuristics include selective attention, memory shortcuts, and rules of thumb.42 Brands can serve as devices that represent larger chunks of information, thereby simplifying information handling and processing. At a minimum, brands should ensure quality, and brand recognition can simplify choice and reduce risk. Whether product-level branding is the best means of serving these functions is, however, questionable.

IT is the lever that could enable a complete rethinking of brand management. By using increasingly economical, IT-based techniques, firms are able to identify customers individually — whether consumers or intermediary customers. Major airlines, direct marketers, such as L.L. Bean and Land’s End, and leading retailers, such as Tesco in the United Kingdom, are already heavily committed to these methods; irrespective of company size or the nature of the industry or product/service, similar IT capabilities exist.43 The revolutionary scenario involves organizing and managing on a customer basis rather than a product basis. As Schultz noted, “Most organizations need a structure that can evolve from brand management into a more practical and forward looking format.”44

Few firms have been built on the basis of “once only” clientele, yet, only recently, have companies begun to realize that they can gain much by considering customers in relational rather than transactional terms. In developing and maintaining customer relationships, a longer term view of an organization’s actions seems both sensible and economically desirable. Service firms have typically cultivated longer term relationships with their customers because they saw better service as a way to retain customers and ward off competition. This is particularly true in industries that require high customer-acquisition spending and a cost structure with disproportionate fixed costs. For example, one Mexican cell-phone company estimates it needs ten years of connection from low-usage-rate customers to break even on them.45 Manufacturers of goods would be prudent to think of the long-term value of consumers: a brand-loyal consumer represents a substantial cash flow.

However, by focusing on the consumer rather than the brand as the “unit of analysis,” we can consider the consumer holistically, i.e., across brands and products. The economics of the relationship change from this perspective: for any multiproduct company, the discounted cash flows of purchasing bundles should be significantly greater. Customer insight about the seller may benefit from a holistic view as well.

Unfortunately, neither brand managers nor firms typically think of customers in this way, i.e., holistically or empathetically. Historically, companies have not cultivated this awareness in development and training courses nor acknowledged it in evaluation and reward systems. A major shift is required to move toward managing customers rather than — or at least as well as — managing brands and products.

By focusing on the customer (instead of products, brands, or geography), a firm’s entire marketing structure changes.46 This structure requires a clear line of authority for every customer, although managers are usually responsible for a group of customers of a determined size and determinable value.47 The appropriate term may be a “portfolio of customers” since it captures the spirit of viewing them as an investment having a lifetime value.48 Officers at Wachovia Bank have long managed this way, perhaps a reason it is one of the most successful “super regionals” in the United States.49

Rather than selling the brand to as many customers as possible, the brand or product manager will play a more supportive role by being a product or brand expert, aiding the firm’s customer-portfolio managers in developing and providing the products and brands needed to increase the lifetime value of their customers. Some brands or products will not be sold to certain customer portfolios (determined by computing the impact on the net value of the customer portfolio). The firm will require customer-portfolio managers to handle its relationships with individual customers in a portfolio, rather than merely requiring brand and product managers to superintend a brand name. No longer will brand managers research markets to identify what a reasonably large segment of “average” customers will want. Nor will they price, promote, and distribute products to best reach the targeted market.

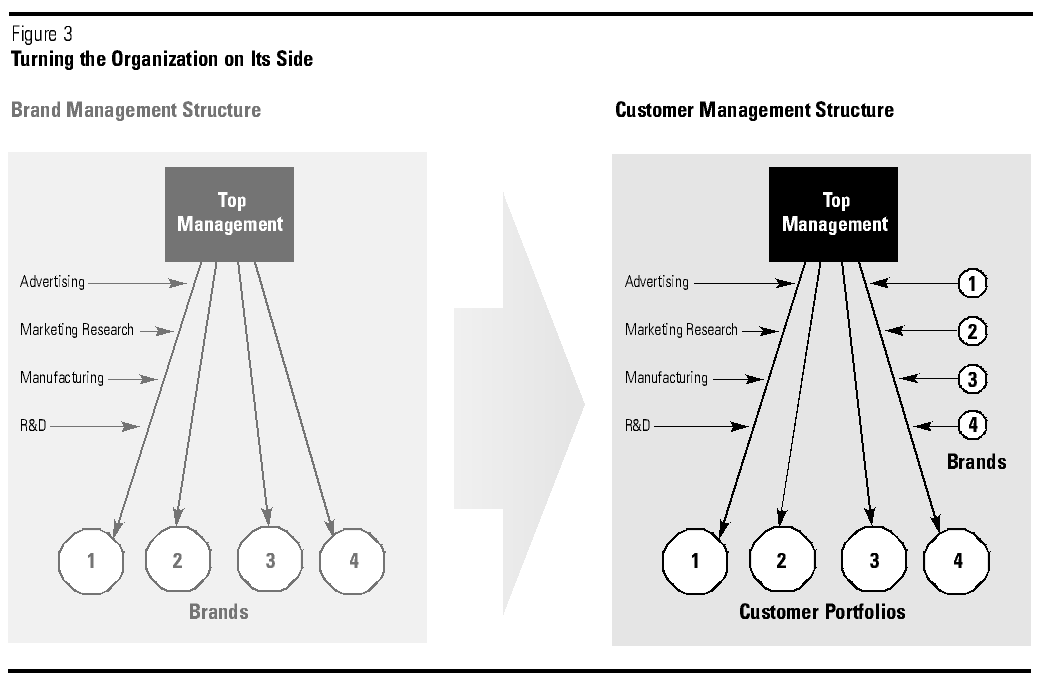

The changes in organizational structure required are quite profound, for they imply quantum shifts in thinking and conceptualization for many branded-goods companies. Rather than turning the organization on its head, the current marketing structure should lie on its side, moving from a brand management structure to a customer-based structure in which the brand manager almost becomes a staff function (see Figure 3).50

{kind=link}

In the brand management structure, brands are the pillars of the firm, with all other functional activities serving them or subordinate to them. In the customer-management structure, customer portfolios are the pillars, with other functions and brands serving them. A significant number of business-to-business marketers have already made this seemingly radical change, and a number of packaged-goods marketers have arranged their trade marketing similarly, shifting their emphasis from brands to categories.

This Peppers and Rogers-like vision requires a significant change, but would be accompanied by a heightened potential for true insights about customers.51 In this scenario, empathetic managers would literally “immerse” themselves in their consumers or buyers.52 Interaction would be continuous and ongoing; product and brand awareness would gradually improve. Personal, multifaceted dialogue may promote a more proactive exchange process in both managers and customers. Cohort matching would become even more important because contact with a specific, assigned manager would become an experience to be carefully engineered.53

Trends Affecting Brand Management

We shall not be so bold as to predict either the pace of change or the particular scenario that may emerge. However, the foregoing discussion suggests a few trends that will influence brand management, irrespective of which scenarios materialize.

Customer and Consumer Focus

Globalization, deregulation, and technology access are driving competitive intensity in market after market, making increased intermediary customer and consumer focus mandatory. The press reports customer-based reorganizations almost daily.54 Research emphasizes the virtue of direct contact with customers.55 Adherents of total quality management preach a similar sermon, while new approaches to marketing research increasingly feature direct customer contact.56 Marketing will move increasingly from “walking around” to “in your face.” This transition will require that the whole organization somehow become committed to focusing on the customer.57

Marketing as a Driver of Innovation

Because intensified competitiveness will more quickly erode competitive advantage, CEOs are paying ever greater attention to the innovation process.58 Although innovation should be construed more broadly, the usual focus is on new product development. Yet, marketers are often less than committed to cooperating with researchers.59 It has been convincingly argued by Simmonds that driving innovation is a key responsibility of marketers, but often other concerns dominate the marketing agenda.60 To meet the challenges of the new millennium, this lack of attentiveness must change.

Adoption of Information Technology

In many companies, marketing practitioners are less than enthusiastic about IT, an attitude that cannot persist. Not only does IT serve as a vehicle of analysis, it permits the maintenance of large-scale customer interaction and enables conversations with customers. IT makes possible integrated supply-chain management, analysis of scanner data, and unprecedented Internet dialogues. Furthermore, IT is the way to implement the shift in focus discussed above. Effective customer service, targeted communication, and managing interactions with proactive customers will require greater IT sophistication among marketers.

Senior Management Involvement

Lest we seem dismal pariahs and critics, we should also lay responsibility for creating enabling conditions where it belongs — with senior management. Changes in strategy, structure, systems, and human-resources management necessitate senior managers’ involvement. In the past, senior management has been widely perceived as tolerating, if not condoning, management practices that risked jeopardizing the shareholders’ interests over the long term. Now the onus is on the managers to ensure that future decisions generate value for both consumers and shareholders.

Under the revolutionary scenario described earlier, senior management must revamp its human resources strategy. Adopting an entirely different approach to the recruitment, selection, training, motivation, and control of customer-portfolio managers may be necessary. A new generation of marketers, who may be drawn from the targeted customer population, may differ greatly from conventional brand managers. Under this scenario, dealing with brand managers who must adjust to changes in the scope of their jobs will require considerable sensitivity.

Conclusions

We view brands from an evolutionary perspective and conceptualize them as a solution to problems or opportunities within the business context. Brands are no longer static “monoliths,” facing survival or extinction. Rather they are dynamically evolving functional patterns.

Although we primarily focused on the management of brands, the key lesson is that managers should focus on the functions of brands rather than on brands themselves. We began by positing the functions that brands fulfill for both buyer and seller, hinting that they perform more functions for the latter than the former. For buyers, brands reduce search costs, reduce perceived risk, and provide socio-psychological reward. It is worthwhile to speculate about performing these functions in other ways. Such an exercise is essential to understanding and shaping how brands will evolve. This type of proactive, creative thinking will enhance the ability of marketing managers to influence their own destiny.

Of course, the three broad scenarios we outline are not mutually exclusive. Managers in different markets will likely enact various aspects. Brands will undoubtedly evolve from the rather static notions prevailing today, but the directions of change are far from fixed. Consumers, trade customers, competitors, and technology will play their respective roles, but the creative input of managers may well be the determining factor in the future of brand management.

References

1. Product and brand management issues remain high on the research priority list of the Marketing Science Institute, although they rank below marketing organization and processes.

Marketing Science Institute, Review (Cambridge, Massachusetts: Marketing Science Institute, Fall 1996).

2. “Death of the Brand Manager,” The Economist, 9 April 1994, pp. 67–68.

3. Throughout the paper, we use the term “customer” inclusively to subsume both the consumer and the trade customer. When discussing one or the other of these specifically, we identify them.

4. See, for comparison:

D. Aaker, Managing Brand Equity: Capitalizing on the Value of the Brand Name (New York: Free Press, 1996); and

P. Doyle, “Building Successful Brands: The Strategic Options,” Journal of Consumer Marketing, volume 7, number 2, 1993, pp. 5–20.

5. K.L. Keller, “Conceptualizing, Measuring and Managing Customer-Based Brand Equity” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 91–123, 1991); and

P.R. Berthon, N. Capon, and J.M. Hulbert, “Everything You Wanted to Know About Branding But Were Afraid to Ask” (University of Wales: Cardiff Business School, working paper, February 1998).

6. For a more detailed exposition on the functions of brands, see:

T. Ambler, “The Case for Branding” (London: London Business School, working paper, Stage 1 Report for CIM, October 1996).

7. G.S. Low and R.A. Fullerton, “Brands, Brand Management, and the Brand Management System: A Critical Historical Evaluation,” Journal of Marketing Research, volume 31, May 1994, pp. 173–190.

8. Harvard Business School, “Procter & Gamble Europe: Vizir Launch (1983)” (Boston: Harvard Business School, Publishing Division, Case 9-384-139, 1983).

9. A. Richards, “What Is Holding Back Today’s Brand Manager?” Marketing, 3 February 1994, pp. 16–17.

10. P. Weisz, “Major Marketers Reorganize Teams,” Adweek, 17 January 1994, p. 14; and

J. Lawrence, “Thinning Ranks at P&G,” Advertising Age, 13 September 1993, p. 2.

11. The Economist (1994).

12. B. Morris, “The Brand’s the Thing,” Fortune, 4 March 1996, pp. 28–38.

13. A.D. Shocker, R.K. Srivastava, and R.W. Ruekert, “Challenges and Opportunities Facing Brand Management: An Introduction to the Special Issue,” Journal of Marketing Research, volume 31, May 1994, pp. 149–158.

14. B. Saporito, “Procter & Gamble’s Comeback Plan,” Fortune, 4 February 1985, p. 30.

15. J. Liesse, “Slotting Bites New Products,” Advertising Age, 5 November 1990, p. 16.

16. R.C. Blattberg and J. Deighton, “Managing Marketing by the Customer Equity Test,” Harvard Business Review, volume 74, July–August 1996, pp. 136–144.

17. See, for comparison:

P.R. Berthon, L.F. Pitt, and R.T. Watson, “The World Wide Web as an Advertising Medium: Towards an Understanding of Conversion Efficiency,” Journal of Advertising Research, volume 36, January–February 1996, pp. 43–53.

18. P. Milgrom and J. Roberts, Economics, Organization and Management (Englewood Cliffs, New Jersey: Prentice-Hall, 1992), pp. 76–77.

19. T. Levitt, “Marketing Success Through Differentiation of Anything,” Harvard Business Review, volume 58, January–February 1980, pp. 83–91.

20. J. Deighton and K. Grayson, “Marketing and Seduction: Building Exchange Relationships by Managing Social Consensus,” Journal of Consumer Research, volume 21, March 1995, pp. 660–676.

21. V. Houlder, “Fingers That Shop Around,” Financial Times, 24 September 1996, p. 14.

22. “Software’s Holy Grail: No-Fuss Clicking Is What Consumers Need Most,” Business Week, 24 June 1996, pp. 50–53.

23. Houlder (1996).

24. We wish to acknowledge the contribution of an anonymous reviewer who pointed out this important shift.

25. L.L. Berry, E.F. Lefkowith, and T. Clark, “In Services, What’s in a Name?” Harvard Business Review, volume 66, number 5, September–October 1988, pp. 28–30; and

Morris (1996).

26. P. Sellers, “Brands: It’s Thrive or Die,” Fortune, 23 August 1993, pp. 32–36;

E. DeNitto, “Economy Puts Focus on ‘Value,’ Heinz Chairman O’Reilly Says, and That’s Bad for Food Brands,” Advertising Age, volume 1, number 4, 26 July 1993, p. 1.

G. Burns, “Restaurants: Bye-bye to Fat Times,” Business Week, 9 January 1995, p. 89;

A. Taylor, “Higher Rewards in Lowered Goals,” Fortune, 8 March 1993, pp. 75–78; and

A.J. Slomski, “Here They Come: Price-Conscious Patients,” Medical Economics, volume 83, April 1996, pp. 40–46.

27. D. Chanil, “A Year of Change,” Discount Merchandiser, January 1996, pp. 10–12.

28. P.R. Dickson, “Toward a General Theory of Competitive Rationality,” Journal of Marketing, volume 56, January 1992, pp. 69–83.

29. E. Tauber, “Brand Leveraging: Strategies for Growth in a Cost-Control World,” Journal of Advertising Research, volume 28, August–September 1988, pp. 26–30.

30. “Make It Simple. That’s P&G’s New Marketing Mantra — and It’s Spreading,” Business Week, 9 September 1996, pp. 56–61.

31. For details about this change in the United States, see:

W.M. Weilbacher, Brand Marketing (Lincolnwood, Illinois: NTC Business Books, 1995).

32. P.W. Dhar, and S.J. Hoch, “Why Store Brand Penetration Varies By Retailer,” Marketing Science, volume 16, number 3, 1997, pp. 208–227.

For example, in the United States, despite a significant increase in retailer concentration, the historical evidence suggests that brand manufacturers were holding their own in power terms, at least until the early 1990s. See:

P.R. Messinger and C. Narasimhan, “Has Power Shifted in the Grocery Channel?” Marketing Science, volume 14, number 2, 1995, pp. 189–223.

Most of the changes we are discussing have occurred since then, although in many cases the trends that spurred the changes were already in place.

33. A. Mitchell, “Managing by Our Shelves,” Marketing Week, 15 July 1994, pp. 30–33.

34. Aaker (1996).

Also see, for example:

L. Leuthesser, “Defining, Measuring and Managing Brand Equity” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 88-104, 1988);

K.L. Keller, “Conceptualizing, Measuring and Managing Customer-Based Brand Equity” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 91-123, 1991); and

R.K. Srivastava and A.D. Shocker, “Brand Equity: A Perspective on Its Meaning and Measurement” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 91-119, 1991).

35. For example:

M. Hammer and J. Champy, Reengineering the Corporation: A Manifesto for Business Revolution (New York: Nicholas Brealy, 1993); and

J.M. Hulbert and L.F. Pitt, “Exit Left Center Stage? The Future of Functional Marketing,” European Management Journal, volume 14, number 1, 1996, pp. 47–60.

36. Hulbert and Pitt (1996).

37. Aaker (1996).

38. Berry et al. (1988).

39. Economic profit is typically defined as operating profit minus a charge for capital used, computed on the basis of the company’s cost of capital.

Assuming an accurate cost accounting system (often a big assumption), economic profit contributes to increase shareholder value.

40. J.N. Sheth and R.J. Sisodia, “Feeling the Heat,” Marketing Management, volume 4, number 2, 1995, pp. 8–23.

41. Harvard Business School, Command Performance: The Art of Delivering Quality Service (Boston, Massachusetts: Harvard Business School Publishing, 1994), pp. 230–249.

42. J.R. Bettman, An Information Processing Theory of Consumer Choice (Reading, Massachusetts: Addison Wesley, 1979).

43. R.C. Blattberg and J. Deighton, “Interactive Marketing: Exploiting the Age of Addressability, Sloan Management Review, volume 33, number 1, Fall 1991, pp. 5–14;

D. Peppers and M. Rogers, The One-to-One Future: Building Relationships One Customer at a Time (New York: Century Doubleday, 1993).

44. D. Schultz, “A Better Way to Organize,” Marketing News, volume 12, 27 March 1995, p. 15.

45. Harvard Business School, “Grupo IUSACELL (A)” (Boston, Massachusetts: Harvard Business School, Case N9-395-028).

46. If a firm were to sell only a limited range of products or brands, this statement would not hold true. The importance of the distinction rises dramatically, however, as the range of products and/or brands increases. Given the size of large companies today and the worldwide trend to consolidate, this shift would have tremendous impact on most large multinationals.

47. At IBM and some other large business-to-business marketers, this shift has already occurred. For details, see:

N. Capon, “Organizing for Global Account Management” (New York: Columbia University Graduate School of Business, working paper, 1998).

48. Our thinking in this regard has been influenced by the terminology of

Peppers and Rogers (1993);

and, to a considerable extent, by Blattberg and Deighton (1996).

49. N. Capon, “Wachovia Bank and Trust Company,” The Marketing of Financial Services: A Book of Cases (Englewood Cliffs, New Jersey: Prentice Hall, 1992), pp. 24–39.

50. For comparison, see:

T. Peters, Thriving on Chaos (New York: Bantam Books, 1987).

51. Peppers and Rogers (1993).

52. Compare: J. Johanson and I. Nonaka, “Market Research the Japanese Way,” Harvard Business Review, volume 65, number 3, May–June 1987, pp. 29–32.

53. L.P. Carbone and S.H. Haeckel, “Engineering Customer Experiences,” Marketing Management, volume 3, number 3, 1994, pp. 8–19;

G.A. Churchill, R.H. Collins, and W.A. Strang, “Should Retail Salespersons Be Similar to Their Customers? Journal of Retailing, volume 51, Fall 1975, pp. 29–42; and

A.G. Woodside and W.J. Davenport, “The Effect of Salesman Similarity and Expertise on Consumer Purchasing Behavior,” Journal of Marketing Research, volume 11, May 1974, pp. 198–202.

54. The New York Times reported on Morgan Stanley’s reorganization, recounting that the firm “is trying to simplify the way it deals with major corporate clients” by grouping together its debt, equity, and investment banking departments into one “client-driven and not product-driven” structure. “Shadowing Industry Trends, Morgan Stanley Creates 2 Big Divisions,” The New York Times, 17 January 1997, p. D1.

55. S.F. Slater and J.C Narver, “Becoming More Market Oriented: An Exploratory Study of the Programmatic and Market-Back Approaches” (Cambridge, Massachusetts: Marketing Science Institute Report No. 91-128, 1991).

56. F. Gouillart and F. Sturdivant, “Spend a Day in the Life of Your Customers,” Harvard Business Review, volume, 72, number 1, January–February 1994, pp. 116–125.

57. Hulbert and Pitt (1996).

58. See, for example:

General Electric Company, “1990 Annual Report of the General Electric Company” (New York: General Electric Company, 1990); and

Procter & Gamble, “1995 Annual Report of Procter & Gamble” (Cincinnati: Procter & Gamble, 1995).

59. “Technology: Quiet Revolution,” Financial Times, 26 March 1996, p. 10.

60. K. Simmonds, “Marketing as Innovation: The Eighth Paradigm,” Journal of Management Studies, volume 23, September 1986, pp. 479–500.