Develop Profitable New Products with Target Costing

With the emergence of the lean enterprise and global competition, companies face ever-increasing competition. To survive, companies must become experts at developing products that deliver the quality and functionality that customers demand, while generating the desired profits.1 One way to ensure that products are sufficiently profitable when launched is to subject them to target costing.2

Target costing is primarily a technique to strategically manage a company’s future profits. It achieves this objective by determining the life-cycle cost at which a company must produce a proposed product with specified functionality and quality if the product is to be profitable at its anticipated selling price.3 Target costing makes cost an input to the product development process, not an outcome of it. By estimating the anticipated selling price of a proposed product and by subtracting the desired profit margin, a company can establish its target cost. The key is then to design the product so that it satisfies customers and can be manufactured at its target cost.

In Japan, lean enterprises have learned to view target costing not as a stand-alone program, but as an integral part of the product development process. To document the “Japanese” approach to target costing, we visited seven companies with mature and effective target costing systems and documented their procedures in depth. The companies we studied were Isuzu Motors Ltd., Komatsu Limited, Nissan Motor Corporation, Olympus Optical Company Ltd., Toyota Motor Corporation, Sony Corporation, and Topcon Corporation.4 While the target costing practices at each company differed, we identified a common underlying generic approach that we document here to give managers a road map for implementing target costing systems.

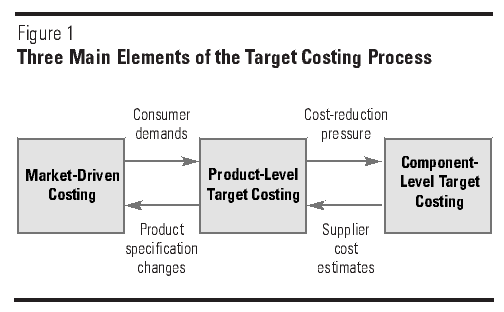

Target costing, to be effective, must be a highly disciplined process. The process used at the seven firms studied can be divided into three sections (see Figure 1). The discipline starts by forcing alignment with the marketplace and requiring a new level of specificity about what customers want and what price they are prepared to pay. Market analysis plays a critical role in shaping the market-driven costing section of target costing by determining so-called allowable costs. Target costing systems use these allowable costs to transmit the competitive cost pressures that the company faces to the product designers. Product-level target costing disciplines and focuses the product designers’ creativity on achieving the cost aspect of this objective. Once a company establishes product-level target costs, it decomposes them to the component level, thus transmitting its cost pressures to its suppliers. Suppliers, in turn, must find ways to design and manufacture the company’s externally sourced components so that they can make adequate returns when they sell their components to the company. Thus, component-level target costing helps discipline and focus suppliers’ creativity in ways beneficial to the buyer.

{kind=link}

While market-driven costing is the first step and should be initiated early in the product conceptualization process, the new product’s design must be sufficiently advanced so that its functionality and quality can be defined adequately to the company’s customers. Otherwise, the customers will not be able to specify a meaningful selling price. Even though the product-level target costing process cannot begin in earnest until the company establishes the allowable cost, the company can start some activities in parallel with the market-driven costing section. For example, it can determine the current cost and initiate some supplier feedback. Furthermore, the ability to fine-tune the functionality and quality of products during product development means that the company has to return to the market occasionally to ensure that design changes have not invalidated the target selling price. Thus, there is iteration between market-driven costing and product-level target costing.

Component-level target costing must begin early during the product-level target costing process since the product-level target cost depends heavily on supplier estimates. However, the formal decomposition process and the establishment of negotiated supplier selling prices occur fairly late in the overall target costing process. The two processes are again iterative, with the product-level target costing process establishing the level of cost reduction that the company’s suppliers must achieve, but ameliorated by the suppliers’ early feedback.

Thus, while product-level target costing is the linchpin of the whole process, a company can manage the three sections predominately in isolation of each other. The chief engineer is responsible for resolving the tensions that are created by the market pressures on the one hand and the suppliers on the other. Effective target costing allows a company to trade off these pressures against each other so that it manufactures and sources products with the required level of quality and functionality and it achieves an adequate return on its investments.

Market-Driven Costing

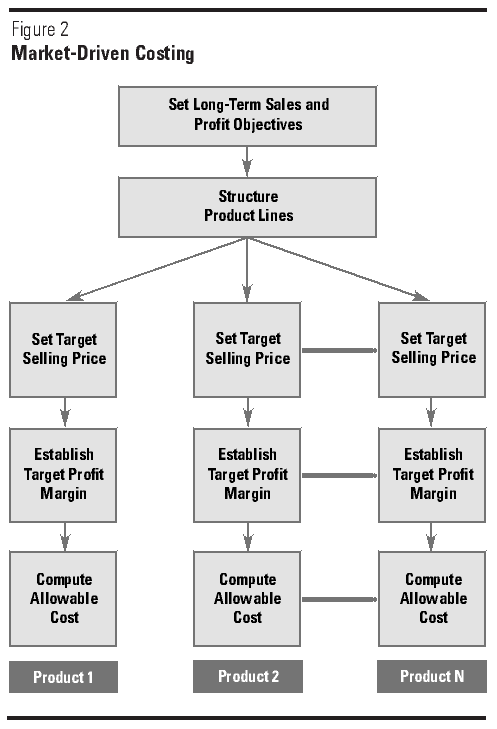

Market-driven costing focuses on customer requirements and uses the concept of allowable cost to transmit the competitive pressure of the marketplace to the company’s product designers and suppliers. We can break market-driven costing into five steps (the first two of these steps cover all the company’s products; the next three are performed for each new product; see Figure 2):

{kind=link}

- Set the company’s long-term sales and profit objec- tives, highlighting the primary role of target costing as a technique for profit management.

- Structure the product lines to achieve maximum profitability.

- Set the product’s target selling price, i.e., the price at which the product is expected to sell when launched.

- Establish the target profit margin the company must earn on the product to achieve its long-term profit objectives.

- Compute the allowable cost by subtracting the target profit margin from the target selling price.

Set Long-Term Sales and Profit Objectives

Target costing begins with the company’s long-term sales and profit objectives. Its primary objective is to ensure that each product, over its life, contributes its planned share of profits to the company’s long-term profit objectives. The credibility of the long-term plan is paramount in establishing target costing discipline. Two factors help establish this credibility. First, the company derives long-term sales and profit plans from careful analysis of all relevant information. To achieve this objective, it spends considerable energy on customer and competitor analysis. For example, Olympus Optical, a manufacturer of cameras and other optical-based products, collects and integrates information from six sources: the corporate plan, a technology review, an analysis of the general business environment, quantitative information about camera sales, qualitative information about consumer trends, and an analysis of the competitive environment.

Second, the company approves only realistic plans. Wishful thinking is not allowed to enter the planning process. For example, at Toyota, Japan’s largest auto manufacturer, the sales division proposes anticipated production volumes based on past sales levels, market trends, and competitors’ product offerings. The sales division typically proposes a figure that is considered achievable. Optimism is thus restrained in favor of realistic goals.

Structure the Product Line

For product lines to be successful, they must be structured carefully to ensure that they satisfy as many customers as possible but do not contain so many products that they confuse customers. For that reason, structuring the product line typically is based on a thorough analysis of how customer preferences change over time. For example, Nissan, Japan’s second largest auto manufacturer, conceptualizes new models by identifying so-called consumer mind-sets. Mind-sets capture how consumers view themselves in relation to their cars. Nissan uses them to identify design attributes that consumers take into account when purchasing a new car. Typical mind-sets include “value seeker,” “confident and sophisticated,” “aggressive enthusiast,” and “budget/speed star.” By detecting clusters of these mind-sets, Nissan can identify niches that contain a sufficient percentage of the auto-purchasing public to warrant introducing a model tailored specifically for that niche.

Set Target Selling Price

The target costing process requires that a company establish a specific target selling price.5 At the heart of the price-setting process is the concept of perceived value. Customers can be expected to pay more for a product than for its predecessor only if its perceived value is higher. For example, at Toyota, the sales divisions usually propose retail prices and sales targets. The fundamental guiding principle they use in setting retail prices is that the vehicle price remains the same unless there is a change in function from the previous model, and this change alters the perceived value of the vehicle in the customer’s eyes. Therefore, increases in retail price are based primarily on the customer’s perception of additional value from new functions, such as the introduction of four-wheel steering (for increased maneuverability) and active suspension, or from better performance, such as higher engine horsepower or better fuel efficiency.

The price increases associated with incremental perceived value are tempered by the availability of competitive products and their perceived value. A company can raise selling prices only if the perceived value of the new product exceeds not only that of the product’s predecessor, but also that of competing products. For example, at Topcon, a manufacturer of ophthalmic instruments and other advanced optics and precision equipment, competitive forces determine the allowable range of market prices. Topcon sets the price of its new products close to its competitors’ prices. However, if managers believe the Topcon product has greater functionality than competitive products, then they will raise the price of the Topcon product. In contrast, if the functionality is perceived to be lower, the price will be correspondingly lower. Once the new product enters the market, competitors usually react by repricing their own products, increasing their advertising levels, or introducing a new model at a lower price.

Given the importance of the target selling price to the whole process, it is not surprising that companies are very careful to ensure the most realistic possible target selling prices. They set the prices by taking into account the market conditions expected when launching the product. For example, Nissan determines the target selling price of a new model by considering a number of internal and external factors. The internal factors include the position of the model in the product matrix and the strategic and profitability objectives of top management for that model. The external factors include the corporation’s image and level of customer loyalty in the model’s niche, the model’s expected quality level and functionality compared to competitive offerings, its expected market share, and the expected prices of competitive models.

Establish Target Profit Margin

The objective in establishing target profit margins is to ensure achievement of the company’s long-term profit plan. Usually, the division in charge of the product line is responsible for achieving the overall profit target. For example, Sony, Japan’s leading manufacturer of consumer electronics, uses an iterative process to set the target profit margin for each product. The starting point is the group profit margin identified by each group’s profit plan. Once the annual group profit target is set, each group is responsible for its own profitability. Two important considerations in setting target profit margins are to ensure that the margins are realistic and that they are sufficient to offset the life-cycle costs of the products.

Set Realistic Profit Margins.

A company can set target profit margins in two ways. In the first method, it starts with the actual profit margin of the predecessor product and then adjusts for changes in market conditions. Nissan adopts this approach when it uses computer simulations to identify the relationship between selling price and profits. From this historical relationship, it identifies the target profit margins of new products, based predominantly on their target selling prices. The aim of this careful analysis is to set realistic profit margins that will enable it to achieve its long-term profit plans.

In the second method, the company starts with the target profit margin of the entire profit line (or other grouping of products) and raises or lowers the target profit margin for individual products, depending on the realities of the marketplace. Sony calculates the first-cut target cost for a new product by subtracting the group target profit margin from the product’s target selling price. It compares the resulting target cost to the estimated cost of the new product. When it considers the target cost too low, it allows the target profit margin to decrease, but only if it can increase another product’s target profit margin sufficiently to offset the loss. The outcome for the product with the decreased target margin is an increased target cost; the outcome for the product with the increased profit margin is a decreased target cost. The objective is to maintain the group’s profit target. When all the individual product decisions are complete, Sony runs a simulation of overall group profitability to make sure the group’s profit target will indeed be met.

Offset for Life-Cycle Costs.

If product launch or discontinuance requires high investments or if a product’s selling prices or costs are expected to change significantly during its life, the company has to adjust the target profit margin accordingly. The purpose of such adjustments is to ensure that the company accounts for all costs and savings when determining the target profit margin so that the expected profitability of the product across its life is adequate.

Without such adjustments, the company risks either launching products that do not earn an adequate return or not launching products that will earn an adequate return over their lives.

Companies with products that require large up-front investments typically analyze their life-cycle profitability. These analyses include a determination of the investment, both capital and marketing related, required to bring the new product to market. The objective of the analyses is to ensure that target profit margins are set large enough so that products will earn an adequate profit margin over their lives (assuming all goes according to plan). For example, when the conceptual design reaches the stage where Nissan can make rough estimates of how many vehicles it is likely to sell and the costs associated with the development of the new products, it undertakes a life-cycle contribution study to estimate the overall profitability of the proposed model. The study compares the estimated revenues generated by the new model to the expected cost of the product across its life.

Companies that can reduce product costs substantially during the manufacturing stage of the product’s life cycle undertake a different life-cycle analysis that reflects any savings in production costs expected during the manufacturing phase in the target costing profitability analysis. For example, the joint impact of increased functionality and reduced prices places severe pressure on Olympus Optical to reduce costs.

Only by continuously taking costs out of products can the company hope to remain profitable. This intense cost reduction across the manufacturing life of the product often reflects the fact that the target selling price already incorporates the anticipated cost savings.

Compute Allowable Cost

Once it has established the target selling price and target profit margin, the company can calculate the allowable cost by simply subtracting the target profit margin from the target selling price:

Given the way in which target profit margins are set, there are two critical issues that a company must understand. First, the allowable cost reflects the company’s relative competitive position because it is based on its realistic, long-term profit objectives. Consequently, the allowable cost is not a benchmark against which the company can measure itself compared to its competitors. To make allowable costs act as benchmarks in this way, target profit margins that reflect the capabilities of the most efficient competitor would have to be set. Second, the allowable cost does not take into account the cost-reduction capabilities of the company’s product designers or suppliers. Therefore, there is no guarantee that the company can achieve the allowable cost. When a product’s allowable cost is considered unachievable, the company must establish a higher cost in the product-level target costing process.

Product-Level Target Costing

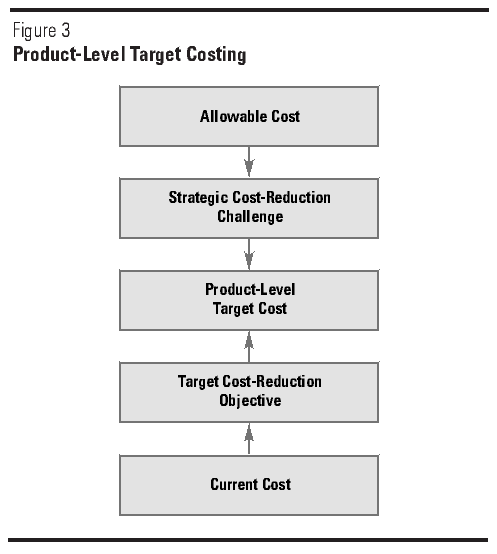

In the second part of the target costing process, product designers focus on finding ways to develop products that satisfy the company’s customers at the allowable cost. In practice, however, it is not always possible for the product designers to find ways to do that. Therefore, the process of product-level target costing increases the product’s allowable cost to a target cost that the company can reasonably expect to achieve, given its capabilities and its suppliers (see Figure 3).

{kind=link}

Product-level target costing can be broken into three steps:

- Set the achievable product-level target cost.

- Discipline the target costing process to ensure that the target cost is met where feasible. 3. Achieve the product’s cost to the target level without sacrificing functionality and quality by using value engineering and other engineering-based cost reduction techniques.

Set Product-Level Target Cost

In highly competitive markets, customers expect each new generation of products to improve, in terms of higher quality and functionality or reduced prices. Any of these improvements, or a combination, requires that the company reduce the costs of new products to maintain its profitability. The degree of cost reduction required to achieve the allowable cost is the target cost-reduction objective, derived by subtracting the allowable cost from the current product cost:

The current cost of the new product is determined by adding up the current manufacturing costs of each major function of the new model, assuming no cost-reduction activities are undertaken. For the current cost to be meaningful, the major functions that the company uses in product construction have to be very similar to those that it will eventually use in the new product. For example, if the existing model uses a 1.8 liter engine and the new model uses a 2.0 liter one, the appropriate current cost is for the most similar 2.0 liter engine that the company produces or purchases.

Since the allowable cost is derived from external conditions and does not take into account the company’s design and production capabilities and its suppliers, the risk is that the allowable cost will not be achievable. In this case, to maintain the discipline of target costing, the company has to identify achievable and unachievable parts of the cost-reduction objective. The achievable or target cost-reduction objective is derived by analyzing the ability of the product designers and suppliers to remove costs from the proposed product. The purpose of the interactive relationships with the company’s suppliers is to allow them to provide early estimates of their products’ selling prices and, when possible, insights into alternative design possibilities that would enable the company to deliver the desired level of functionality and quality at reduced cost. The product-level target cost is then determined by subtracting the new product’s target cost-reduction objective from its current cost:

Negotiations with the chief engineer and the product designers and major suppliers establish the product-level target cost. All concerned should consider the target cost-reduction objective achievable. It is the number to which the designers will be held accountable for the rest of the project.

The unachievable part of the cost-reduction objective is called the strategic cost-reduction challenge, which is the difference between the allowable cost and the target cost:

It identifies the profit shortfall that will occur when the product designers are unable to achieve the allowable cost, and signals that the company is not as efficient as demanded by competitive conditions. To maintain the discipline of target costing, the company must manage the size of the strategic cost-reduction challenge carefully. The challenge should reflect the company’s true inability to match its competitors’ efficiency. To ensure that this requirement is met, the company must set the target cost-reduction objective so that it is achievable only if the entire organization makes a significant effort to achieve it. If it sets the target cost-reduction objective consistently too high, it will not only subject the workforce to excessive cost-reduction objectives, risking burn-out, but also lose the discipline of target costing as it frequently exceeds its target costs. On the other hand, if it sets the target cost-reduction objective too low, the company will lose competitiveness because new products will have excessively high target costs. Typically, in a company with a well-established target costing system, the strategic cost-reduction challenge will be small or nonexistent, and intense pressure will be brought on the design team to reduce it to zero.

The company establishes the strategic cost-reduction challenge through negotiations between the chief engineer and senior managers. Senior managers push for the smallest number possible, while the chief engineer pushes for a number high enough to ensure that the product-level target cost is achievable. Since the target cost-reduction objective and the strategic cost-reduction challenge add up to the gap between the current cost and the allowable cost, these negotiations maintain the pressure on the product designers to reduce costs. The chief engineer must ensure that the pressure does not become excessive. Thus, when a strategic cost-reduction challenge emerges, the process of setting product-level target costs becomes iterative, with the chief engineer in the middle and senior management and the product designers at the ends.

The emergence of a strategic cost-reduction challenge is a sign for all involved in the new product development to create additional pressure on the product designers and the company’s suppliers to reduce the challenge to zero for the product’s next generation. Thus, the primary purpose of the strategic cost-reduction challenge is to give the company breathing room, while maintaining the overall cost-reduction pressure. If the company cannot reduce the challenge to zero for the next-generation product, it may no longer be fully competitive.

The value of differentiating between the allowable cost and the target cost lies in the discipline that it creates. Target costing systems derive their strength from the application of the cardinal rule: “The target cost must never be exceeded.” If a company continuously sets overaggressive target costs, it would commonly violate the cardinal rule and lose the discipline of the whole process. Even worse, if a company knows the target cost is unachievable, the design team might give up even trying to achieve it and never effectively reduce costs. To avoid this, companies frequently set target costs higher than the allowable costs that are achievable only with considerable effort.

Theoretically, the cardinal rule should relate to the allowable cost. However, companies often have to launch products for strategic reasons, such as to maintain a complete product line. If, early in the target costing process, the company determines that the allowable cost is unachievable, setting a lower target cost allows the product to be launched while maintaining intense pressure to reduce costs. The degree to which the allowable cost is relaxed to produce an achievable target cost is the strategic cost-reduction challenge.

Discipline the Product-Level Target Costing Process

Once the company has established the target cost-reduction objective, it can begin the process of designing the product so that it can be manufactured at its target cost. The chief engineer and his or her superiors must continuously monitor the design engineers’ progress toward this objective. This monitoring ensures that the company can take corrective actions as early as possible and that it doesn’t violate the cardinal rule.

Apply the Cardinal Rule.

The cardinal rule of target costing — “The target cost must never be exceeded” — is critical to ensuring that the discipline of target costing is maintained throughout the design process. The cardinal rule is enforced in three ways. First, whenever improvements in the design result in increased costs, the company must find alternative, offsetting savings elsewhere in the design. Second, the company does not launch products whose costs exceed the target. Finally, the company carefully manages transition to manufacturing to ensure that it achieves the target cost.

The cardinal rule ensures that all involved realize that failure to achieve the product-level target cost will typically lead to cancellation of the project. In a well-disciplined target costing program, few projects will be canceled for failure to achieve the target cost. However, as new product development by its very nature must push technologies and manufacturing processes to their limits, occasional failures occur. These failures are very different from those encountered in non-target–costing environments, where the product is designed to have excessive functionality for its sustainable selling price and, hence, is withdrawn before (or, even worse, after) launch.

Sometimes a company has to apply the cardinal rule in a more sophisticated way than the conventional, single-product perspective. When a given product leads to increased sales of other products, a company must adopt a multiproduct perspective; when it is expected to lead to sales of future generations of products, the company must adopt a multigenera-tional perspective. Only when getting the product to market on time is so critical that cost is of secondary consideration should the cardinal rule be violated. For example, the Walkman market is so competitive that failure to release a timely new model typically will result in considerable lost sales. Sony believes it is imperative to release products on a timely basis and does not allow product redesign to extend product launch dates, even if profitability is below minimum. When such a product is launched, it undergoes two analyses: a thorough review of the design process to identify why the target cost was not achieved and an intense cost-reduction effort immediately after its launch so that the violation of the cardinal rule is as short-lived as possible. The two analyses maintain the discipline of target costing despite the temporary violation.

Achieve the Target Cost

Once a company has established the target cost-reduction objective, it must find ways to achieve it. Several engineering techniques can help product designers reduce product costs, including value engineering (VE), design for manufacture and assembly (DFMA), and quality function deployment (QFD). VE is a multidisciplinary approach to product design that maximizes customer value; it increases functionality and quality while reducing cost. In contrast, DFMA focuses on reducing costs by making products easier to assemble or manufacture, while holding functionality at specified levels. QFD provides a structured approach to ensure that customer requirements are not compromised during the design process.

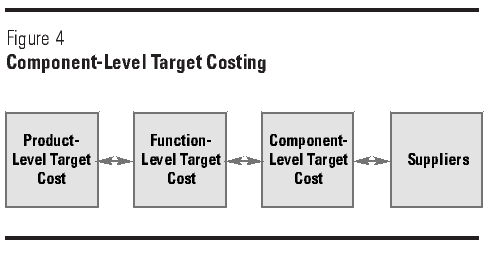

Component-Level Target Costing

Once a company has established a product’s target cost, it develops target costs for the product’s components. This component-level target costing process enables the company to achieve the second objective of target costing: transmitting the competitive cost pressure it faces to its suppliers (see Figure 4). This objective is critical in lean enterprises, which are horizontally rather than vertically integrated. Such companies purchase a significant portion of their materials and parts from external instead of internal suppliers. For example, at Toyota, third-party suppliers are responsible for approximately 70 percent of the parts and materials required to produce the company’s cars. This high level of dependency on externally supplied items makes supplier relations extremely important to Toyota’s success. In particular, the cost and quality of third-party-supplied parts is considered critical.

{kind=link}

Component-level target costing consists of three steps:

- Decompose the product-level target cost to the major function level. Major functions are the sub-assemblies that provide the functionality that enables the product to achieve its purpose. For example, major functions for a vehicle include the engine, transmission, cooling system, air conditioning system, and audio system.

- Set component-level target costs.

- Manage suppliers.

Decompose Target Costs of Major Functions

Identifying major functions allows the design process to be broken into multiple, somewhat independent tasks. Typically, the design of each major function is the responsibility of a dedicated team. Design teams usually include representatives from a number of disciplines, such as product design, engineering, purchasing, production engineering, manufacturing, and parts supply. The overall responsibility for coordinating the design of a new product typically rests with the chief engineer or product manager, who selects the distinctive theme of the new product and sets its functionality. At Toyota, more than 100 engineers from various divisions work with a chief engineer on a typical project, but since they belong to different divisions, not all team members are under his direct supervision. In this sense, the chief engineer is more a project leader than a supervisor of product development.

The chief engineer is responsible for setting the target cost of each major function, usually through an extended negotiation process with the design teams. The target costs typically are based on historical cost- reduction rates. Some companies use relatively simple heuristics to establish the cost-reduction objectives; for example, if the cost of a major function historically has been decreasing by 5 percent a year, then this rate will usually be used. Other companies, including Komatsu, have more sophisticated approaches, such as functional analysis and productivity analysis.

However, not all companies rely solely on historical cost-reduction rates. Some use market analyses to help set the target costs of new products. These market-based approaches are particularly applicable when new forms of product functionality are being introduced. For example, Isuzu uses monetary values or ratios to help set the target costs of major functions and asks customers to estimate how much they are willing to pay for a given function. These market-based estimates, tempered by other factors, such as technical, safety, and legal considerations, often lead to adjustments to the prorated target costs. For example, if the prorated target cost for a component is too low to allow a safe version to be produced, the component’s target cost is increased, and the target cost of the other components is decreased to compensate.

The chief engineer may modify the target costs derived from either historical rates or market analysis for three major reasons. First, if the sum of all the historical rates does not give the desired cost-reduction objective, the chief engineer will negotiate with the head of the design teams of the major functions for higher rates of cost reduction. These negotiations continue until the sum of the target costs of the major functions equals the target cost of the product. Second, if the relative importance of a given major function changes from one generation to the next, the chief engineer will modify the target costs accordingly. For example, if the chief engineer wants the new vehicle to be sportier, he or she might increase the target cost of the corresponding major functions to make it easier for the design teams to achieve both their functionality objective and target cost. However, under the cardinal rule of target costing, these cost increases would have to be offset elsewhere in the design. Third, when the technology on which a major function relies changes, the historical cost-reduction rate of the old technology ceases to be meaningful. Instead, the company should figure in the historical rate for the new technology, if it is available. When entirely new technologies are used, the cost-estimation problem becomes more difficult because no historical data on cost-reduction trends have been developed.

At some Japanese firms, a safety factor, often called “the reserve for the production manager,” is built into the development of major function-level target costs. The purpose of this reserve is to allow for any (minor) cost overruns due to design-related problems that may occur during the production process. Experience has shown that minor overruns are common in practice and cannot easily be avoided. By establishing an adequate reserve, a company can significantly reduce the number of minor cardinal rule violations without reducing the overall discipline of target costing. It creates the reserve by setting the component target costs and assembly and indirect manufacturing target costs so that they add up to an amount below the product-level target cost. The chief engineer is responsible for creating a reserve that is sufficient to offset the anticipated overruns, but does not introduce slack into the production process. The magnitude of the reserve is based on experience from similar product development projects; it is typically quite small, ranging from 5 percent to 10 percent of the product-level target cost.

Once a company has established the target costs of the major functions, it decomposes them to the group component and parts level as appropriate. The objective is to set a purchase price for every externally acquired component.

Set Target Costs of Components

Typically, the major function design teams decompose the target cost of the major function to the component level. At Toyota, each design division is responsible for attaining its respective cost-reduction goal. The specifics of parts, materials, and machining processes are left to their discretion. The chief engineer will sometimes specify cost-reduction targets for specific parts to the related divisions, especially for large, costly parts. These part-specific targets are set at the same time as the divisional targets.

Manage Suppliers

Supplier management has two primary aspects that are particularly important in the component-level target costing process:

- Selecting suppliers.

- Rewarding suppliers for finding creative ways to reduce costs of the components they supply.

Select Suppliers.

A critical decision to be made during the component-level costing process is the sourcing of components. The target costs for externally acquired components are typically set through negotiation. This process starts with suppliers, both internal and external, providing estimates of their selling prices to the company. At Nissan, the first step in the product development stage is to prepare a detailed order sheet for the new model, which lists all the components required. Nissan analyzes it to see which components are likely to be sourced internally and which externally and gives both internal and external suppliers a description of each component and its potential production volumes. Suppliers then provide price and delivery-timing estimates.

The comparison of the target cost of each major function and the sum of the expected costs of the components in that function after cost reduction indicates whether each major function can be produced at its target cost. When the sum of the component costs is too high, additional cost reductions are identified until the total target cost of the representative variation, the one expected to sell the highest volume, is achieved. The target costs for all components are compared to the suppliers’ quoted prices. If satisfactory, the company accepts the quote. If the initial quote is too high, the company undertakes further negotiations until reaching an agreement.

To maintain discipline, a company can relax target costs of components only under very special circumstances and typically for a short period of time. The objective of this relaxation is to allow the supplier to make a reasonable return, while finding ways to reduce costs to the target levels.

Reward Supplier Creativity.

Many companies use incentive plans to encourage their suppliers, both to reward innovation and to signal where additional cost reduction should occur. These plans reward the supplier with all or part of the order for a given component. For example, under its incentive plan, if Nissan accepts a cost-reduction idea, it awards the supplier that suggested it a significant percentage of the contract for that component for a specified time, say 50 percent for twelve months. This incentive scheme is particularly important because even if a cost-reduction objective cannot be achieved for this model, it signals to the suppliers that when the next model is developed, this component will be subject to cost-reduction pressures.

Even with the discipline of target costing, the lowest-cost or highest-value supplier does not always win the bid. Companies actively manage their suppliers to ensure that they remain both efficient and innovative. Isuzu, although it generally gives the order to the supplier rated as having the highest value, often awards companies with a reputation for being good suppliers at least part of the order, even if their products do not have the highest value. Isuzu awards partial contracts to maintain relationships with these companies.

Conclusion

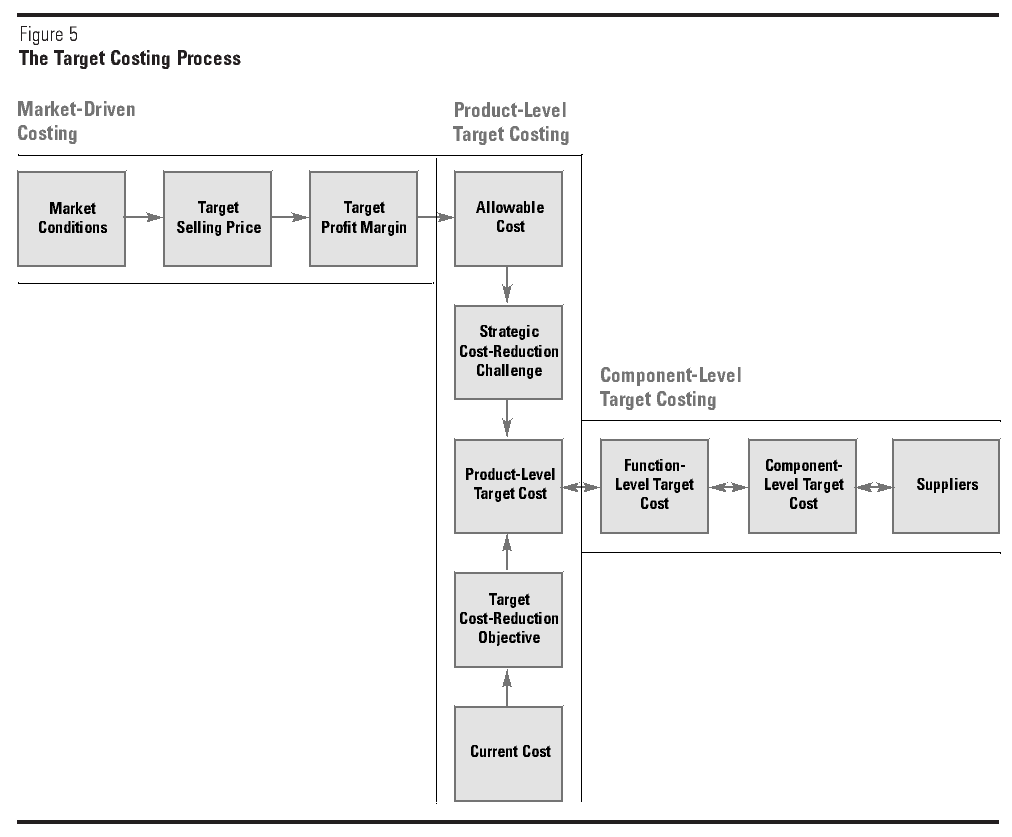

Given a highly competitive environment, companies must manage costs aggressively if they are to survive. Cost management must start at the earliest stages of a product’s life because the ability to change the product significantly increases the degree to which costs can be reduced. Three target-costing processes together discipline the product development process to help ensure that only profitable products are launched (see Figure 5).

{kind=link}

Leading Japanese manufacturers have used target costing systems to their advantage, and western companies are introducing this proactive cost management technique to discipline their product development processes. Target costing and value engineering provide considerable payoffs to early adopters. The company that can most rapidly reduce costs of new products without having to compromise on quality and functionality will gain market share and experience economic success.

References

1. R. Cooper, When Lean Enterprises Collide: Competing Through Confrontation (Boston: Harvard Business School Press, 1995), p. 7.

2. R. Cooper and R. Slagmulder, Target Costing and Value Engineering (Portland, Oregon: Productivity Press, 1997).

3. Target costs should include any costs that are driven by the number of units sold. For example, if the company accepts responsibility for disposing of a product at the end of its useful life, these costs are included in the target cost. See:

R. Cooper and B. Chew, “Control Tomorrow’s Costs through Today’s Designs,” Harvard Business Review,volume 74, January–February 1996, pp. 88–97.

4. R. Cooper and T. Yoshikawa, “Isuzu Motors, Ltd.: Cost Creation Program” (Boston: Harvard Business School, case study 9-195-054);

R. Cooper, “Komatsu, Ltd. (A): Target Costing System” (Boston: Harvard Business School, case study 9-194-037);

R. Cooper, “Nissan Motor Company, Ltd.” (Boston: Harvard Business School, case study 9-194-040);

R. Cooper, “Olympus Optical Company, Ltd. (A): Cost Management for Short Life-Cycle Products” (Boston: Harvard Business School, case study 9-195-072);

R. Cooper, “Toyota Motor Corporation” (Boston: Harvard Business School, case study 9-197-031);

R. Cooper, “Sony Corporation: The Walkman Line”(Boston: Harvard Business School, case study 9-195-076); and

R. Cooper, “Topcon Corporation: Production Control System” (Boston: Harvard Business School, case study 9-195-082).

5. When firms sell the same product at different prices, for example, in different countries or through different channels, an average selling price is used.